Yen Plunge: Oil & Fed Policy Drive USD/JPY Surge Past 159

The JPY Exchange Rate continues its depreciation trajectory against the USD, driven by persistent central bank divergence and Japan's fundamental...

The Catalyst: Dissecting the News

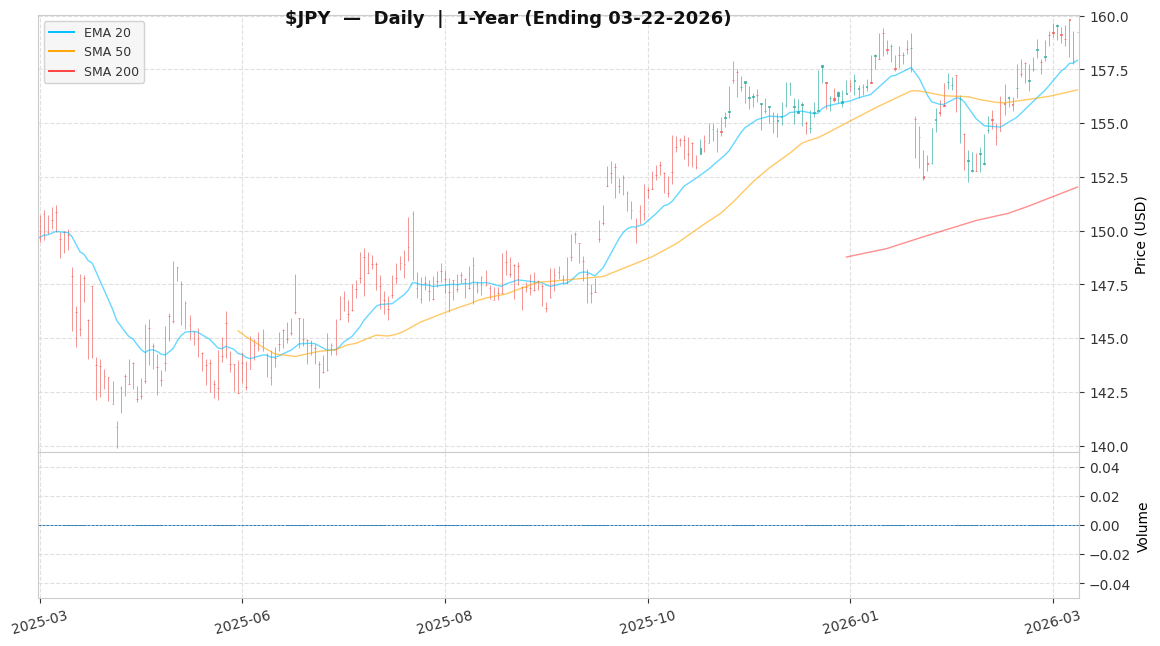

The primary catalyst for the JPY Exchange Rate’s recent weakness stems from the confluence of rising global oil prices, with Brent crude topping $111 a barrel, and sustained central bank policy divergence between the Federal Reserve and the Bank of Japan. This exacerbates Japan’s trade balance deficit given its heavy reliance on energy imports, while the Fed’s decision to hold rates steady, alongside building wholesale inflation pressures in the US (accelerating to 3.4%), has effectively reined in market bets on aggressive rate cuts, maintaining a significant yield differential in favor of the USD. The USD/JPY pair surged past 159.35, nearing the critical 160 level and marking a >2% depreciation since late February — after touching that high, the pair has pulled back to the current 157.76 level, consolidating near multi-month highs as markets reassess intervention risk while the underlying macro drivers remain firmly in place.

Core Logic & Growth Drivers

The primary driver for the JPY Exchange Rate’s directional bias remains the stark monetary policy divergence between the Bank of Japan and the Federal Reserve, anchoring the USD/JPY pair’s upward momentum. The current approximately 500 basis point policy rate differential between the Fed’s target range and the BOJ’s near-zero stance continues to drive strong carry interest in the USD/JPY, further amplified by Japan’s structural vulnerability to elevated oil prices, which directly impacts its terms of trade and consequently, the yen’s value. While the BOJ’s cautious stance on tightening implies minimal near-term domestic cost pressures for funding, the overarching global macro environment dictates the USD/JPY’s trajectory. The JPY faces persistent headwinds from a stronger dollar index, which remains near its highest levels in four months, coupled with a higher bar for direct intervention from the Ministry of Finance given that current yen weakness is largely fundamentally driven by oil prices and rate differentials. My bear trigger for the JPY Exchange Rate would be if the USD/JPY pair decisively breaks below the 155 level, or if the Bank of Japan delivers an unexpected hawkish shift that significantly narrows the rate differential with the Federal Reserve.

The Financial Reality

The USD/JPY trades at 157.76, currently 1.28% off its 52-week high of 159.82 and well above its low of 139.89. The substantial interest rate differential between the Federal Reserve and the Bank of Japan underpins the current carry dynamic, with the US policy rate significantly above Japan’s near-zero stance. Market positioning suggests a continued bias towards USD strength given the persistent yield advantage and the yen’s role as a funding currency in times of relative calm. 1-month implied volatility in USD/JPY reflects elevated market uncertainty around potential Japanese intervention and the trajectory of global oil prices, which directly impacts Japan’s trade balance. One structural tail risk worth monitoring: a domestically driven wage-inflation cycle in Japan — where rising real wages sustain household price expectations above the BOJ’s target — would raise the probability of a BOJ pivot, narrowing the rate differential and challenging the current carry trade dynamic.

Actionable Strategy

I’m assigning the JPY Exchange Rate ($JPY) a ‘Tactical Buy’ rating for the USD/JPY pair over the next 12-18 months. This represents a tactical overweight position in my portfolio, not a permanent core holding — sized to reflect the scenario-based nature of the targets rather than a high-conviction fundamental bet. With roughly equal (~33%) probability weighting across scenarios, the probability-weighted expected return is approximately ~1.7% (= (+3.0% + 7.0% − 5.0%) ÷ 3), reflecting a positive expected return under equal-weight scenario assumptions, though targets are scenario-based, not fundamentally anchored. My Base Case target for USD/JPY is 162.50, representing a +3.0% upside scenario from the current market price of 157.76 as of 2026-03-22. As a currency pair, targets are scenario-based rather than derived from fundamental multiples. My Bull Case target is 168.81, representing a +7.0% upside scenario from current levels, driven by a further widening of US-Japan rate differentials or a sustained surge in global energy prices that further deteriorates Japan’s terms of trade. My Bear Case target is 149.87, representing a -5.0% scenario-based decline if the USD/JPY pair decisively breaks below the 155 level, or if the Bank of Japan delivers an unexpected hawkish shift that significantly narrows the rate differential with the Federal Reserve, at which point I would re-evaluate the position for a potential reduction. The key macro indicators I will monitor each quarter to track this thesis: the US-Japan 2-year yield spread, Brent crude price trajectory, and any shifts in the Bank of Japan’s forward guidance — each of which I expect to confirm the current divergence before considering any position expansion. Given the modest probability-weighted return of ~1.7%, this is best sized as a tactical FX overlay rather than a high-conviction standalone bet — position weight should reflect the scenario-based, not fundamental, nature of the targets. Given the typical use of leverage in FX trading, position sizing and margin discipline are critical — a decisive move through the 155 bear trigger level could quickly erode carry gains and accelerate losses beyond the stated -5.0% scenario target. Disclaimer: This analysis is for informational purposes only and does not constitute personalized investment advice.