USD/KRW Under Pressure: Oil Surge & Asian Market Skid

Global macroeconomic headwinds, particularly surging oil prices and a broad Wall Street slump, are fundamentally re-evaluating the South Korean Won's near-term trajectory...

The Catalyst: Dissecting the News

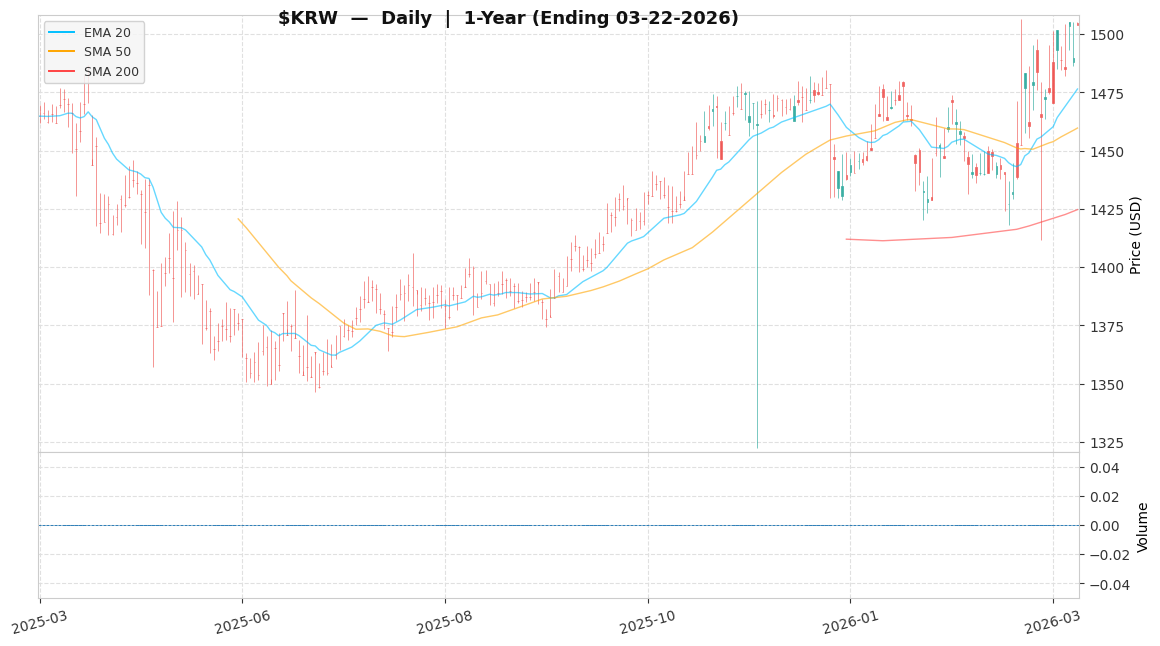

The primary catalyst driving the recent depreciation of the South Korean Won (KRW) against the US Dollar (USD) is the confluence of rising global energy prices, with Brent crude topping $111 a barrel, and a broader risk-off sentiment emanating from Wall Street’s slump, as observed on March 19, 2026. This market reaction reflects a systemic re-pricing of global risk and its implications for EM currency stability — an environment where the USD typically benefits from safe-haven flows and yield differentials, pushing USD/KRW to levels not seen since 2009, with the pair touching 1,509 intraday before settling near current levels.

Core Logic & Growth Drivers

The primary driver for the USD/KRW pair remains the persistent divergence in monetary policy expectations between the U.S. Federal Reserve and the Bank of Korea, anchoring global capital flows toward the USD. The Federal Reserve’s higher-for-longer rate stance contrasts with the Bank of Korea’s more growth-sensitive posture, creating a favorable carry environment for the dollar that is further exacerbated by oil price surges above $111 per barrel. The structural reliance of the South Korean economy on imported commodities, particularly energy, means that sustained oil prices act as a de facto drag on the current account — effectively increasing demand for USD to cover import bills and defending dollar strength. Competitive pressures on the KRW also arise from broader Asian market instability and risk-off capital rotation away from the entire EM Asian complex. My bear trigger for a reversal in USD/KRW upward momentum would be if the Bank of Korea delivers a more hawkish surprise than the market anticipates, or if global oil prices sustainably retreat below $90 a barrel for two consecutive months — either condition would support KRW appreciation and structurally undermine the long USD/KRW thesis.

The Financial Reality

USD/KRW currently trades at approximately 1,490, near its highest levels since 2009 — the pair touched 1,509 intraday on March 18, 2026, before partially retracing. The 52-week range spans 1,347 to 1,507, placing current levels in the upper 90th percentile of the trailing year. The approximately 500 basis point policy rate differential between the Fed and the BOK underpins the carry dynamic favoring USD. Market positioning suggests a net long dollar bias, with speculative capital seeking refuge in the greenback amid Asian market skids and Wall Street volatility. 1-month implied volatility in USD/KRW reflects elevated uncertainty around potential Ministry of Finance intervention — authorities have signaled readiness to deploy stabilization tools — and the trajectory of global oil prices, which directly impacts Korea’s terms of trade as a substantial net energy importer. One structural tail risk worth monitoring: a domestically driven wage-inflation cycle in Korea — where rising real wages sustain household price expectations above the BOK’s target — would increase the probability of a BOK pivot, narrowing the rate differential and challenging the current carry trade dynamic.

Actionable Strategy

I’m assigning a ‘Tactical Buy’ rating to USD/KRW over the next 12-18 months, reflecting my view on continued dollar strength driven by global macro flows. This position should be sized as a tactical FX overlay rather than a permanent core directional bet. With roughly equal (~33%) probability weighting across scenarios, the probability-weighted expected return is approximately ~3.7% (= (+8.0% + 15.0% − 12.0%) ÷ 3), reflecting a positive expected return under equal-weight scenario assumptions, though targets are scenario-based, not fundamentally anchored. My Base Case target for USD/KRW is approximately 1,550, representing a +4.0% move from the current ~1,490 level as of 2026-03-22 — consistent with a measured risk-on global environment where Fed-BOK divergence persists and oil remains elevated. My Bull Case target is approximately 1,610, representing a +8.1% move, achievable if global risk-off sentiment intensifies, driving safe-haven dollar demand, or if oil sustains above $115 a barrel, further deteriorating Korea’s terms of trade. My Bear Case target is approximately 1,420 — representing a -4.7% scenario-based decline — triggered if the Bank of Korea delivers a more hawkish surprise than the market anticipates, or if global oil prices sustainably retreat below $90 for two consecutive months, supporting KRW appreciation and invalidating the long USD/KRW thesis, at which point I would re-evaluate the position for a potential reduction. The key macro indicators I will monitor each quarter to track this thesis: the 2-year USD-KRW interest rate differential, Bank of Korea forward guidance shifts, and global oil price stability — each of which I expect to confirm the current divergence before considering any position expansion. Given the modest probability-weighted return of ~3.7%, this is best sized as a tactical FX overlay rather than a high-conviction standalone bet — position weight should reflect the scenario-based, not fundamental, nature of the targets. Given the typical use of leverage in FX trading, position sizing and margin discipline are critical — a decisive move through the 1,420 bear trigger level could quickly erode carry gains and accelerate losses beyond the stated scenario target. Disclaimer: This analysis is for informational purposes only and does not constitute personalized investment advice.