Urgent PLTR Alert: Palantir's Explosive Risks Uncovered

Palantir Technologies Inc. ($PLTR) is a high-growth, high-risk asymmetric bet — a selective, limited Accumulate only for institutional capital with strict sizing discipline.

Investment Highlights

U.S. commercial revenue surged 137% Y/Y in Q4 2025, validating AI platform adoption.

Palantir reported 70% Y/Y total revenue growth in Q4 2025, exceeding expectations.

Valuation is extreme at 70.1x Non-GAAP forward P/E (~125–145x on a GAAP-adjusted basis including SBC) and ~43x forward P/S.

This is a HIGH-risk Accumulate (Selective · Non-core Satellite Position) — maximum 3% portfolio weight with strict entry discipline. This is not a core holding.

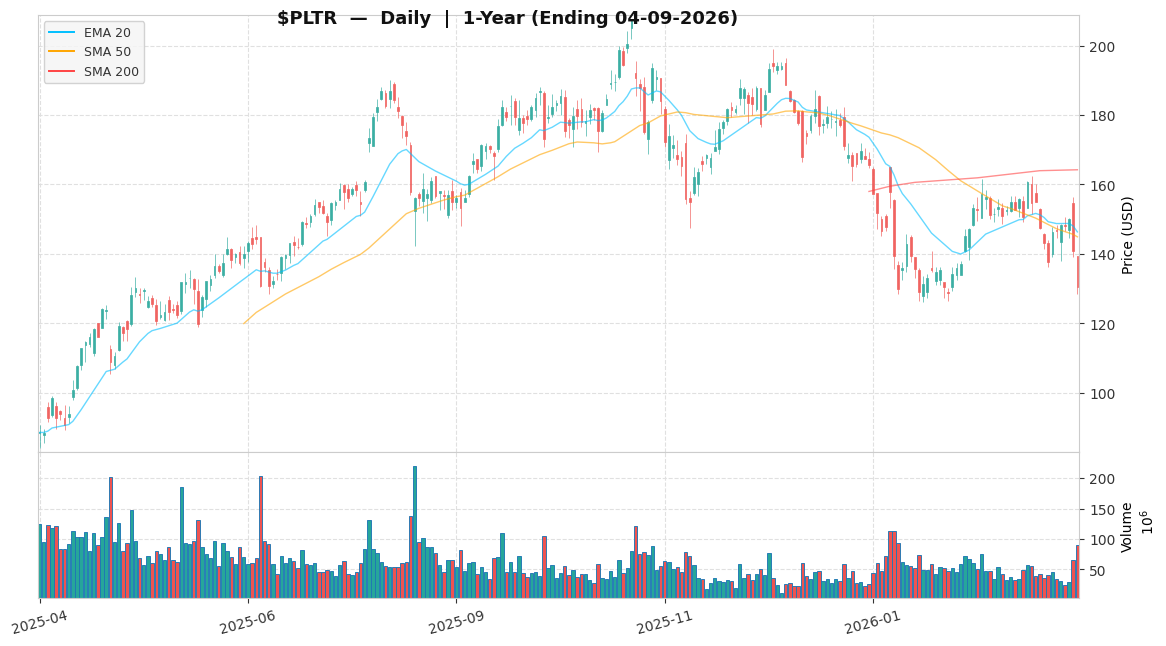

Palantir Technologies Inc. ($PLTR) presents a high-growth, high-risk asymmetric structure: exceptional AI-driven momentum offset by extreme valuation and binary execution risk. The Accumulate (Selective) rating is not a broad buy signal — it is a risk and position-sizing framework for patient institutional capital that can tolerate a -25% standard bear case and a -50% tail scenario. The stock’s -37.1% drawdown from its 52-week high of $207.52 reflects heightened risk from AI agent disruption, increased scrutiny of AI vendor data security in government contract pipelines, and macro headwinds driving sector-wide multiple compression, creating a potential entry point in the $115–$130 range for disciplined buyers.

The Catalyst: Dissecting the News

The primary catalyst and price action context are summarized in the Investment Highlights above. See the Actionable Strategy section for scenario-based price targets and risk triggers.

Core Logic & Growth Drivers

Palantir Technologies Inc. ($PLTR) is primarily driven by its expanding AI platforms across both U.S. government and commercial sectors. Street consensus forecasts 2026 revenue of $7.182–$7.198B — approximately 61% YoY growth. U.S. commercial revenue surged 137% YoY in Q4 2025, signaling strong AI platform adoption. We estimate this segment still represents a mid-single-digit percentage of total revenue — a meaningful re-rating CATALYST, not yet the primary earnings driver for the current fiscal year.

Critical but under-discussed risk: Palantir’s Stock-Based Compensation (SBC) — historically ~25–30% of revenue — creates meaningful GAAP/Non-GAAP divergence. Investors relying solely on adjusted EPS risk overstating true economic earnings power. For intrinsic value purposes, we model SBC as a full economic cost on GAAP FCF.

Palantir’s operating cash flow of $2.13B (TTM) provides ample liquidity for continued AI investment, with accretion to EPS modeled by late 2027. The company faces increasing competitive pressure from Microsoft Azure and Google Cloud; production ramp execution remains a key operational risk. Our variant view: the Street is underestimating accelerated AI agent adoption potential. Bull Thesis Impairment Trigger: U.S. Commercial Revenue Growth sustained below 100% YoY for two consecutive quarters.

Competitive Moat — Why PLTR Commands a Premium vs. Azure/Google: Palantir’s premium-to-peers multiple is frequently challenged by pointing to Microsoft Azure and Google Cloud as cheaper alternatives for enterprise AI workloads. This comparison misses three structural differentiators that hyperscalers structurally cannot replicate: ①Classified and air-gapped data environments — Palantir holds accreditations to operate inside classified government networks where commercial cloud providers are legally barred; this is a regulatory moat, not a technical one. ②The Ontology architecture — 20+ years of engineering investment to create semantic cross-dataset connections between operational, financial, and intelligence data silos; no single-year build can replicate this structural depth. ③Mission-critical 3–7 year contract structures — government contracts at this level carry renewal mechanisms and embedded switching costs that create revenue predictability unavailable to commercial SaaS peers. These moats partially justify the ~43x forward P/S premium to the SaaS Rule of 40 cohort (15–25x), but they are neither infinite nor immune to budget policy shifts — which is precisely why the DOGE risk deserves elevated weight in this analysis.

The Financial Reality

Palantir Technologies Inc. ($PLTR) is priced at $130.49, approximately 37.1% below its 52-week high of $207.52 and 73.5% above its 52-week low of $75.22.

Valuation Context — Multiple Expansion Justification: The elevated 70.1x Non-GAAP forward P/E reflects a growth premium. To assess whether multiple expansion to 78.9x (Base) or 94.7x (Bull) is justified, we apply two standard high-growth benchmarks: - Rule of 40: With 61% revenue growth guidance and ~35% adjusted operating margin target, PLTR scores approximately 96 on the Rule of 40 — extraordinary by any standard. SaaS companies with Rule of 40 scores above 60 typically command 15–25x forward revenue. At ~43x forward P/S, PLTR trades at a 1.7–2.9x premium to this range, partially justified by its government moat and AI differentiation, though with limited margin of safety. - PEG Ratio: At 70.1x forward P/E against estimated NTM EPS growth of ~30–35%, PLTR’s PEG of approximately 2.0–2.3x sits at the upper bound of historical high-growth SaaS ranges (typically 1.0–2.5x), suggesting multiple expansion requires consistent outperformance, not just in-line results.

Historical Multiple Bands & Peer P/S Context: PLTR’s current ~70x Non-GAAP forward P/E and ~43x forward P/S must be read in historical context. In 2022, the stock reached a 30x P/E trough during the broad tech de-rating. Through 2023–24, it recovered to a normalized 50–70x range as government contract momentum re-emerged. In 2021, it peaked above 150x P/E during the speculative bubble. Today’s 70x sits at the upper end of the normalized range — not bubble territory, but with materially higher absolute EPS stakes than in prior cycles. On P/S, Datadog trades at ~15–20x and MongoDB at ~12–15x, both with strong Rule of 40 scores. PLTR’s ~43x represents a 2.1–3.6x premium to these AI-infrastructure comps — defensible via the classified-data moat, but carrying compression risk if that moat faces budget policy headwinds. Key framing: a reversion to 50x P/E (our bear case boundary) implies roughly -29% from current levels. This is not a hypothetical — it is exactly where the stock found support in 2023.

GAAP vs. Non-GAAP Alert: Applying SBC of ~25–30% of revenue as a full economic cost, we estimate GAAP-adjusted NTM EPS of approximately $0.90–1.05, implying a GAAP forward P/E of ~125–145x — roughly 2x the reported Non-GAAP multiple. That is the earnings multiple institutional buyers must fully underwrite.

Revenue Mix Sensitivity (DOGE Stress Test): Assuming approximate 2025E revenue splits of 55% government / 45% commercial, a DOGE-driven deceleration in U.S. government revenue growth to 10% would require commercial to grow ~156% YoY to defend 2026 guidance — above the current 137% trajectory, requiring further acceleration. At 30% government growth (our bear trigger), commercial requires ~119% YoY — within the current trajectory and therefore manageable. The 119% scenario is the realistic stress; the 156% scenario is where the thesis begins to break. This asymmetry confirms U.S. government revenue velocity is the single most important near-term watchpoint.

Debt/Equity: At 3.06%, financial leverage risk is minimal. A payback period analysis on the $2.13B TTM operating cash flow indicates AI infrastructure investments carry an estimated 2–3 year return horizon — note this is not a full DCF; a proper discounted cash flow model incorporating WACC, terminal value, and SBC-adjusted free cash flow would be required for an intrinsic value estimate. Our forward model projects an increasing mix shift toward higher-margin software solutions as a structural driver of operating margin expansion toward 35%+ by FY2026 — contingent on continued AIP platform scale — a working structural assumption, not an established fact.

Actionable Strategy

We assign Palantir Technologies Inc. ($PLTR) an “Accumulate (Selective)” rating for the next 12–18 months: maximum 3% portfolio weight; initiate a 1/3 starter position now; add only on pullbacks to $115–$120 (approaching the 200-day moving average).

Rating vs. PWR Reconciliation: The 7.5% PWR falls below the 10–15% institutional hurdle typically required for HIGH-risk single stocks. The Accumulate (Selective) rating coexists with this gap for three reasons: ①the 3% portfolio cap limits maximum mark-to-market loss to a manageable level even at the bear extreme ($65.10); ②this is structured as an asymmetric satellite bet on AI platform re-rating, where non-linear option value is partially outside the linear PWR framework; ③the “Selective” qualifier is structural, not decorative — it means KPI-conditional additions only, strict entry criteria, and no size-up without thesis confirmation. Investors who cannot tolerate the full bear range ($65–$98) should not initiate this position.

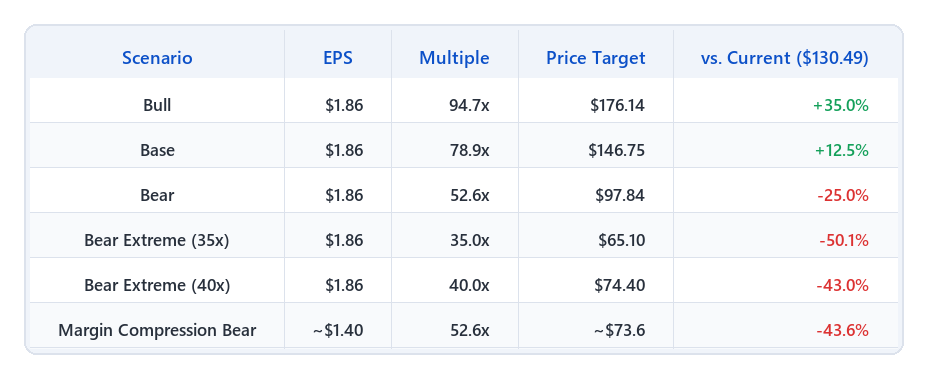

Scenario Summary (all targets derived from $1.86 NTM EPS per FactSet consensus, 2026-04-09):

PWR: ~7.5% (= +12.5% × 33% + 35.0% × 33% − 25.0% × 33%)

Primary KPI Trigger Framework: Decision priority: U.S. commercial revenue growth and U.S. government revenue growth are the two metrics that drive actual portfolio action. Margin and SBC KPIs are supplementary early-warning signals — important context, not primary exit triggers. Threshold rationale: 100% marks the minimum growth rate consistent with the bull AI-monetization narrative; 80% signals material deceleration; 60% indicates structural breakdown well below the valuation premium’s required growth floor. The 30% government threshold reflects normal contract execution versus DOGE-disrupted procurement.

Three-Tier KPI Trigger Framework:

| Trigger Level | U.S. Commercial Revenue Growth | Action | |---|---|---| | Bull Thesis Impairment | Below 100% YoY for 2 consecutive quarters | Re-evaluate bull case; no new adds | | Position Reduction | Below 80% YoY for 2 consecutive quarters | Trim to 1.5% portfolio weight or less | | Full Exit | Below 60% YoY for 2 consecutive quarters | Exit position; thesis invalidated |

| Trigger Level | U.S. Government Revenue Growth | Action | |---|---|---| | Government Watch | Below 30% YoY for 1 quarter | Heightened monitoring | | Government Exit | Below 30% YoY for 2 consecutive quarters | Stop-loss or significant position reduction |

Supplementary Profitability KPIs (monitor alongside primary triggers):

| Trigger Level | Profitability KPI | Action | |---|---|---| | Margin Watch | Adjusted Operating Margin below 25% for 2 consecutive quarters | Re-evaluate margin expansion thesis; no new adds | | SBC Escalation Flag | SBC as % of revenue increases QoQ for 2 consecutive quarters | Flag as additional valuation risk multiplier; review position size |

We apply equal 33%/33%/33% probability weights because current data does not provide sufficient conviction to skew toward either the bull or bear scenario — the AI agent monetization catalyst and government contract erosion risk are symmetrically uncertain. Our analytical lean favors base over bear given PLTR’s demonstrated commercial momentum; however, equal weights are applied as a deliberate risk-management discipline to avoid optimism bias in portfolio sizing. PWR and portfolio rationale are detailed in the Rating vs. PWR Reconciliation box above.

Our Base Case target is $146.75, derived from a 78.9x P/E on NTM EPS of $1.8600 per FactSet consensus as of 2026-04-09, representing a +12.5% move. The 78.9x vs. current 70.1x expansion is justified by the Rule of 40 score of ~96 and PEG of ~2.1x — both at the high end of historical SaaS premium ranges, but defensible if US commercial revenue re-accelerates.

Our Bull Case target is $176.14, applying 94.7x to an expanded EPS estimate assuming adjusted operating margin exceeds 35%, suggesting +35.0% upside. At 94.7x, we approach the upper bound of high-conviction AI software comps; this multiple requires sustained 120%+ commercial growth and government stability.

Our Bear Case target is $97.84, applying a compressed 52.6x multiple — which is near the 50x threshold we consider the inflection point between “AI premium justified” and “full de-rating.” Bear Extreme Scenario: A macro regime shift combined with AI monetization disappointment could compress multiples to the 35–40x range: at 35x × $1.86 NTM EPS = $65.10; at 40x × $1.86 = $74.40. These are not hypothetical — PLTR traded at a 30x P/E trough in 2022, and the 35–40x zone represents a full return to pre-AI-premium normalization. We treat this as a tail risk requiring the 60% commercial growth exit trigger to materialize. Margin Compression Sub-Scenario: If competitive pressure or higher CapEx forces adjusted operating margin down to 25–28% from the guided 35%+ target, forward EPS declines to approximately ~$1.40 (vs. consensus $1.86). At the standard bear multiple of 52.6x, this yields a target of ~$73.6 — within the bear extreme zone and achievable without any multiple compression whatsoever. Even at the current 70.1x forward P/E with zero multiple compression, $1.40 EPS implies ~$98 — the standard bear case target, reached purely from earnings disappointment. See the Scenario Summary table above for complete reference. Key exit triggers: U.S. Commercial Revenue growth below 60% for two consecutive quarters, OR valuation overextending beyond 100x forward P/E without corresponding EPS growth. Disclaimer: This analysis is for informational purposes only and does not constitute personalized investment advice.

🛡️ Key Institutional Risks

AI Monetization & Growth Deceleration Palantir’s premium valuation is predicated on aggressive AI-driven growth. If 2026 revenue growth falls below the guided 61% YoY, or U.S. commercial revenue growth decelerates below the 100% Bull Thesis Impairment Trigger, it signals a failure in AI monetization and could trigger a re-rating. Below 80% triggers active position reduction; below 60% triggers full exit. MITIGATION: Monitor quarterly earnings for U.S. commercial revenue growth rates against the three-tier trigger framework above. Apply GAAP FCF (including SBC as full cost) rather than Non-GAAP metrics when assessing intrinsic value.

Government Contract Erosion & DOGE Spending Risk A substantial portion of Palantir’s revenue comes from U.S. government contracts. The DOGE-driven federal spending review represents a specific, underappreciated near-term risk: if AI procurement budgets are cut, U.S. government revenue growth (currently ~55% YoY) could fall below the 30% trigger threshold, and — per our revenue mix simulation — would require commercial revenue to grow 156% YoY to defend guidance alone. Both metrics must be tracked simultaneously. MITIGATION: Track DOGE budget revision disclosures and government contract renewal rates. Implement a stop-loss or trim if U.S. government revenue growth falls below 30% for two consecutive quarters. Cross-reference against commercial growth trajectory to assess total revenue defense capability.

Extreme Valuation & GAAP-Adjusted Multiple Compression At 70.1x Non-GAAP forward P/E and ~125–145x on a GAAP basis (after applying SBC as a full economic cost), PLTR is highly sensitive to any negative news or sentiment shifts. High SBC (25–30% of revenue) creates a hidden valuation risk: Non-GAAP multiples understate the true economic cost, and any multiple compression from 70x toward the 50x “AI premium boundary” would imply a -25%+ move. MITIGATION: Track both GAAP and Non-GAAP metrics. Set maximum acceptable Non-GAAP forward P/E. If SBC as % of revenue increases quarter-over-quarter, flag as an additional valuation risk multiplier.

🔴 OVERALL RISK RATING: HIGH Rationale: 70.1x Non-GAAP forward P/E (~125–145x GAAP), 37% drawdown already absorbed, binary AI monetization thesis, and DOGE government risk collectively warrant HIGH classification. MODERATE is appropriate for stocks at or below 30x forward earnings with predictable revenue.

📅 Next check-in: Q2 2026 earnings