Uber's Nvidia Alliance: The Structural Bear Case for Tesla's Robotaxi

Why Uber’s 18.4x forward P/E offers a mispriced entry into the AV network duopoly, and why Tesla's vertically integrated moat is showing cracks.

The Catalyst: The “Asset-Light” Syndicate vs. The Walled Garden

The recent Nvidia GTC announcement is not merely a PR exercise; it signals a structural regime shift in the autonomous vehicle (AV) landscape. Uber ($UBER) and Nvidia are establishing an “asset-light compute + distribution” syndicate that directly challenges Tesla’s ($TSLA) capital-intensive, vertically integrated Robotaxi thesis. While Tesla burns billions on Dojo compute and relies strictly on its proprietary fleet data, Uber provides the exact missing piece that hardware manufacturers desperately need: an active, global, high-liquidity two-sided marketplace. Nvidia supplies the silicon and AV stack, allowing Uber to remain a pure aggregator without holding depreciating metal on its balance sheet. This effectively bifurcates the market—Tesla’s hardware-first walled garden versus the Uber/Nvidia open ecosystem.

Valuation & Justified Trading Targets

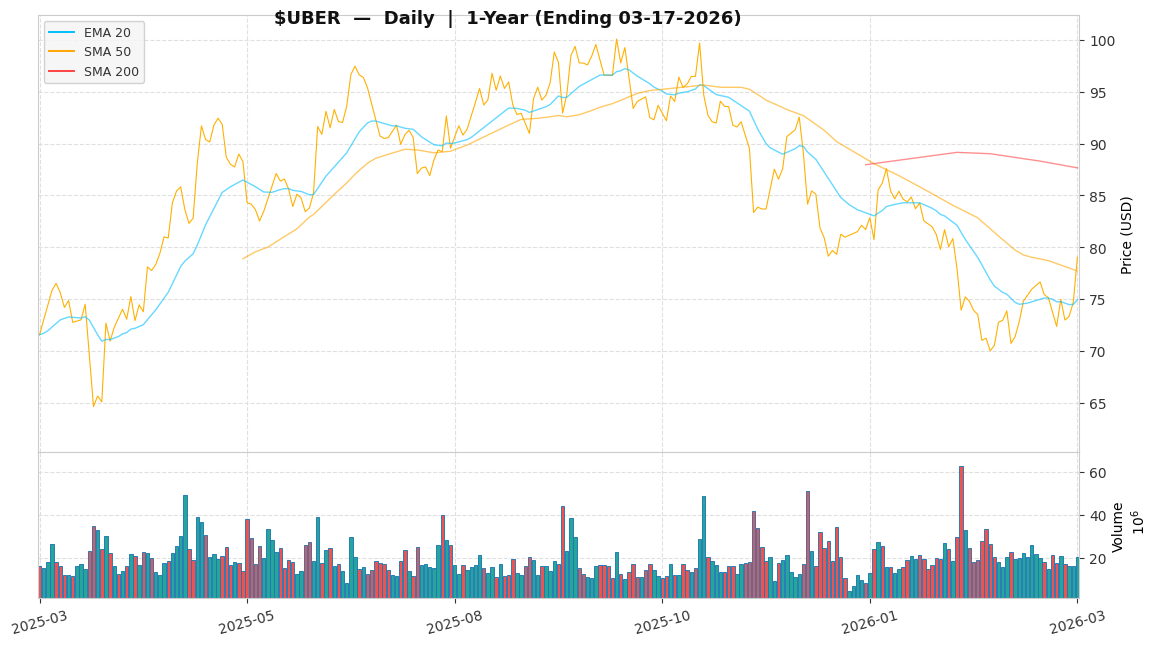

Trading at $78.97 with a forward P/E of 18.4x and TTM revenues of $52.0 billion, $UBER is currently priced as a mature mobility and delivery utility. The market is assigning virtually zero premium for L4/L5 AV network domination. This is a mispricing. As Uber slowly transitions from a human-driven variable cost model to an AV-routed software-as-a-service (SaaS) platform, we model a structural margin accretion well beyond its current 19.3% profit margin.

The Trade: We initiate a tactical long at $75 (a historical volume node and fundamental floor supported by core mobility cash flows). Our target is a multiple re-rating to 24x forward P/E as the software-margin mix increases, implying a price target of $105 over a 12-18 month horizon. A strict stop-loss is set at $65; a break below this level invalidates the base-case mobility growth thesis and implies a reversion to a 15x multiple, reflecting a purely commoditized transport business.

Risk Decomposition: What Breaks the Thesis?

However, institutional capital must price in three distinct risk vectors before allocating:

Capex & Unit Economic Reality: Uber’s 43.8 D/E ratio is healthy precisely because it is asset-light. The primary risk is that OEM partners balk at the economics, forcing Uber to finance and own the Nvidia-equipped hardware fleets themselves. If Uber shifts from an aggregator to a fleet owner, Return on Invested Capital (ROIC) will collapse.

Regulatory & Antitrust Friction: The CPUC and NHTSA have already demonstrated hostility toward Waymo and Cruise incidents. Scaling AVs in tier-1 cities will face brutal municipal headwinds, potentially delaying the software-margin realization by 24-36 months.

Macroeconomic Sensitivity: At its core, the current $52B revenue run-rate is highly sensitive to consumer discretionary spending. A rate-driven hard landing could crush core mobility cash flows before the AV narrative has time to materialize, triggering a severe near-term drawdown.