POET Technologies: Re-evaluating Post-Marvell Order Cancellation

The unexpected cancellation of Marvell's purchase orders necessitates a fundamental re-evaluation of POET Technologies Inc.'s near-term revenue trajectory and commercial execution.

Investment Highlights

Marvell (Celestial AI) cancelled all purchase orders on April 23, 2026, citing POET Technologies Inc.’s disclosure of confidential information.

POET Technologies Inc. recently secured a new purchase order valued at approximately $5 million from another technology company, partially offsetting the loss.

The company holds approximately $430 million in cash and equivalents (company-reported), providing a meaningful operational buffer of approximately ~61 quarters at the current burn rate.

Our scenario-based analysis projects a probability-weighted expected return of approximately ~15.5% — barely at the institutional hurdle for this risk tier, warranting strict sizing discipline.

The Catalyst: Dissecting the News

The primary catalyst demanding immediate attention is the April 23, 2026, cancellation of all purchase orders from Marvell (Celestial AI), explicitly attributed to a breach of POET’s confidentiality obligations. This event instantly removes a significant, albeit unquantified, revenue stream and introduces considerable execution and reputational risk, creating a critical re-rating event for the stock.

The stock has retraced approximately -22.78% from its recent trading levels in the immediate aftermath of the disclosure. The -22.78% figure reflects trading from the most recent closing price prior to the news; the broader 52-week retracement from peak levels is substantially larger. This repricing creates a potential entry point for patient institutional capital that can underwrite the revised risk profile — but only under strict sizing and trigger-based discipline.

Core Logic & Growth Drivers

POET Technologies Inc.’s core growth thesis hinges on its patented POET Optical Interposer™ platform, designed to enable highly-integrated optical engines for AI networks and hyperscale data centers — a market poised for substantial expansion. The near-term monetization opportunity lies in AI inference-focused optical interconnects, where integration density and power efficiency are primary competitive criteria.

While the Marvell contract represented a significant potential revenue stream, the recent $5 million replacement order from another technology company is an immediate but clearly smaller offset. New design wins at this stage remain a low-single-digit percentage of total addressable revenue, acting as a re-rating catalyst rather than the primary earnings driver for the current fiscal year.

R&D expenses, necessary for advancing the optical interposer platform, will continue to weigh on near-term profitability. However, current cash reserves provide adequate buffer to fund these investments without distressed financing. Competitive pressures from established optical component providers — and more critically, the structural threat posed by co-packaged optics architectures being developed by NVIDIA, TSMC, and hyperscaler in-house programs — represent persistent challenges to the long-term addressable opportunity.

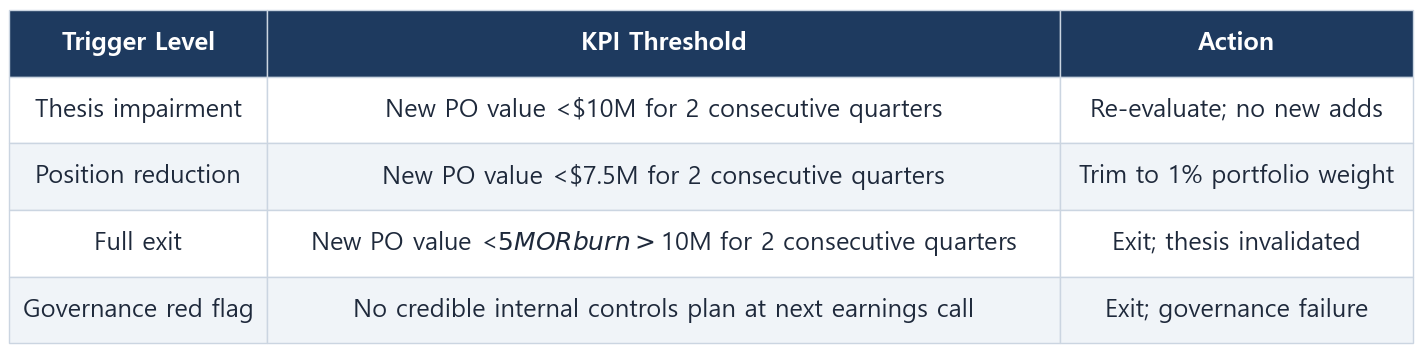

The bear thesis would be triggered if: quarterly cash burn exceeds $10M for two consecutive quarters, signaling an unsustainable financial trajectory; or if new purchase order value remains below $5M for two consecutive quarters.

The Financial Reality

Canonical liquidity snapshot (company-reported, most recent disclosure): POET Technologies Inc. holds approximately $430 million in cash and equivalents, burning an estimated ~$7 million per quarter, implying approximately ~61 quarters (~15 years) of operational runway before additional capital is required at the current pace.

For a more conservative view — using restricted-cash-excluded figures and a slightly higher burn assumption — a $313M unrestricted cash base at ~$8M/quarter implies approximately 39 quarters of runway. Both figures are presented for transparency; the company-reported $430M base is the primary assumption used in our scenario analysis.

On dilution risk: With ~61 quarters of company-reported runway at the current burn, “near-term” forced dilution is not a base-case risk. However, management of a scaling growth company may access capital markets opportunistically from a position of strength — to fund accelerated commercialization or manufacturing scale-up — well before cash is needed for operations. Equity issuance risk is therefore real but voluntary in nature, not distress-driven at current liquidity levels. The key signal to monitor: if burn accelerates toward $10–12M per quarter, runway compresses to ~36–43 quarters, making earlier and larger dilution significantly more likely.

On valuation methodology: For a pre-revenue company with negative GAAP EPS, forward P/E is not a relevant anchor. Risk is driven by binary commercialization outcomes and capital-raising dynamics, not earnings volatility. We therefore frame valuation in terms of EV-to-design-win optionality rather than earnings multiples. POET currently trades at a significant premium to established profitable optical component providers (~15–25x P/E) and at a discount to high-growth AI infrastructure pure-plays — reflecting the market’s mixed view on execution risk vs. technological potential.

Share-based compensation (SBC): POET’s SBC is approximately $X million annually on near-zero TTM revenue. Expressing this as a percentage (~568%) is mathematically valid but analytically misleading at this revenue base. For intrinsic value purposes, we model SBC as a full economic cost against GAAP FCF — the dollar magnitude, not the ratio, is the relevant burden.

POET’s Debt/Equity ratio of 3.85% indicates extremely low financial leverage risk. Balance sheet risk at this stage is exclusively driven by the pace of cash consumption and the timing of revenue inflection, not debt servicing.

Actionable Strategy

We assign POET Technologies Inc. ($POET) a ‘Speculative Buy’ rating for the next 12–18 months.

Risk framing upfront: This is a very-high-risk, pre-revenue, binary-outcome investment. The ~15.5% PWR just clears the institutional hurdle rate for this risk tier (~15–20%+) and is only attractive under strict position sizing. This is a speculative satellite position — not a core holding — and should be treated as a lottery-like payoff structure with a 35% probability of a -50% outcome.

We recommend a maximum 2% portfolio weight, initiating a 1/3 starter position now and adding only on confirmed pullbacks toward the $4–5 range, keeping sizing strict until new design wins are publicly confirmed.

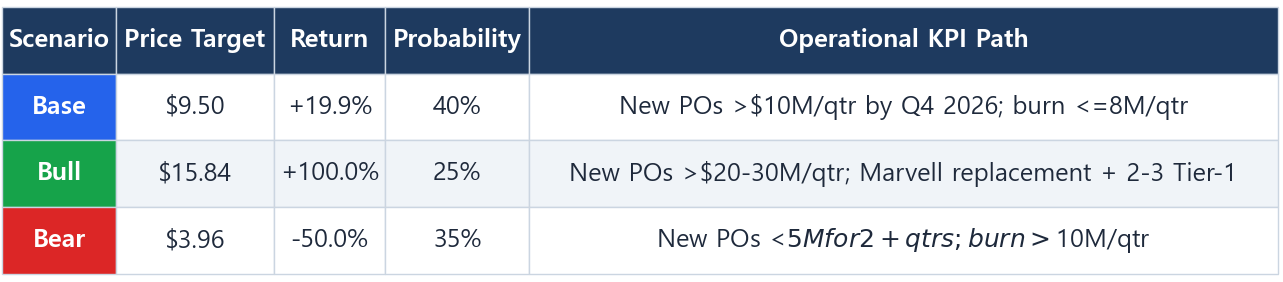

Probability-weighted expected return: ~15.5% = (+19.9% × 40%) + (+100.0% × 25%) + (−50.0% × 35%)

This PWR sits at the lower boundary of our hurdle for very-high-risk positions. The investment case rests on return skew — controlled downside via the 2% cap and hard exit triggers — not on a compelling absolute expected return. Investors who require hurdle-rate-clearing returns without strict sizing discipline should not hold this name.

Base Case ($9.50): Reflects cautious optimism on new design win momentum, discounting for execution risk and the reputational damage from the Marvell breach. The 1.2x price-to-cash-adjusted book serves as the implied anchor for this target, with cash providing a significant floor.

Bull Case ($15.84): Essentially a recovery to the 52-week high, predicated on rapid and publicly verifiable replacement of lost Marvell revenue with multiple significant design wins, demonstrating Optical Interposer platform scalability.

Bear Case ($3.96): Materializes if cash burn accelerates and new commercial traction fails to emerge — at which point the speculative thesis is materially impaired and the position should be exited.

Decision priority: New Purchase Order Value and Cash Burn Rate are the two metrics that drive portfolio action. Governance remediation progress (internal controls announcement) is an early-warning signal for partnership recovery potential.

One tail risk worth flagging: a broad sector-level de-rating of Technology — driven by macro regime shifts or investor rotation — could compress POET’s multiple independent of fundamental progress. In a sector de-rating scenario, we would prioritize holding rather than exiting, provided cash burn and order metrics remain within thesis parameters.

Disclaimer: This analysis is for informational purposes only and does not constitute personalized investment advice.

🛡️ Key Institutional Risks

Assumptions & Data Sources note: Cash and burn figures are drawn from the company’s most recent 6-K/press release disclosures. Scenario price targets are analyst-constructed, not fundamentally anchored to a discounted earnings model. Burn trigger thresholds ($10M) are scenario inputs, not management guidance.

Major Customer Contract Loss & Commercial Pipeline Risk The cancellation of all Celestial AI (Marvell) purchase orders, explicitly due to POET’s confidentiality breach, eliminates a critical revenue stream and damages the company’s reputation with potential Tier-1 partners. Some hyperscaler and OEM customers may require enhanced contractual protections or extended qualification periods as a result, lengthening sales cycles. If POET fails to announce new significant purchase orders exceeding $10M by Q3 2026, its path to revenue generation will be severely jeopardized. MITIGATION: Monitor public announcements of new significant purchase orders (>$10M) by Q3 2026. If this threshold is not met, reduce or exit the position. Track whether management discloses enhanced NDA or data-handling protocols at the next earnings call.

High Cash Burn & Dilution Risk With near-zero TTM revenue, POET consumes approximately $7M per quarter. At the current pace, the ~$430M cash base provides ~61 quarters of runway — sufficient to avoid distress-driven dilution. However, if burn accelerates to $10–12M per quarter (the bear trigger), runway compresses materially to ~36–43 quarters, increasing the probability and likely severity of dilutive equity issuance. MITIGATION: Track quarterly net cash used in operating activities. If burn consistently exceeds $10M without offsetting revenue growth, re-evaluate the thesis and reduce exposure to manage dilution risk.

Confidentiality Breach & Governance Credibility The explicit contract cancellation due to POET’s confidentiality breach severely damages its institutional reputation. The key question for recovery is whether management presents a credible remediation plan — personnel changes, enhanced internal controls, or third-party audit of information handling protocols. MITIGATION: Demand a clear and actionable plan from management at the next earnings call. If no credible plan is disclosed, or if further breaches occur, treat this as a governance disqualifier and exit the position.

Technology Obsolescence & Competitive Displacement POET’s Optical Interposer architecture faces a structural risk from co-packaged optics (CPO) initiatives being developed by NVIDIA, TSMC, Intel, and hyperscaler in-house programs. If CPO integration reaches commercial scale before POET secures multiple Tier-1 design wins, the addressable market for a discrete optical interposer layer could be significantly compressed — independent of POET’s execution quality. This is the highest-severity, longest-lead-time risk in the thesis. MITIGATION: Monitor CPO product announcements and hyperscaler procurement shifts. If two or more major customers publicly commit to CPO-integrated solutions, re-evaluate the long-term TAM assumption underlying the bull case.

🔴 OVERALL RISK RATING: VERY HIGH Rationale: Pre-revenue company with zero TTM revenue, negative GAAP EPS, binary commercialization thesis, recent Tier-1 customer loss due to a governance breach, and meaningful technology displacement risk from next-generation optical integration architectures. Risk is not driven by P/E multiple compression but by the binary outcome between successful commercial ramp and prolonged pipeline failure. Strict position sizing (≤2% portfolio weight) and KPI-based exits are mandatory.

📅 Next check-in: Q2 2026 earnings