NIKE's Q4 Warning: Decoding the 14% Stock Plunge

NIKE, Inc.'s Q4 guidance indicates near-term headwinds from inventory cleanup and restructuring, necessitating a re-evaluation of its immediate growth...

Investment Highlights

NIKE, Inc.’s Q4 revenue guidance projects a 2%-4% decline, missing consensus expectations.

Greater China sales are expected to be down ~20% in FQ4, signaling significant regional challenges.

“Win Now” actions aim for long-term health but create near-term margin and revenue pressure.

The stock’s recent -13.98% 5-day price change creates a potential entry point for patient capital.

The Catalyst: Dissecting the News

The primary catalyst for NIKE, Inc. ($NKE)’s recent price action is its significantly softer-than-expected FQ4 revenue guidance, projecting a decline of 2% to 4%, starkly missing the consensus expectation for a 1.9% increase, signaling ongoing operational challenges as the company executes its “Win Now” restructuring actions. The -13.98% drawdown in five days, and a more significant -44.9% decline from its 52-week high of $80.17, directly reflects this earnings revision and persistent macro headwinds, creating a potential entry point for patient institutional capital to evaluate the trough.

Core Logic & Growth Drivers

The core growth thesis for NIKE, Inc. centers on its brand strength and innovation pipeline, which the Street generally expects to drive low-single-digit revenue growth despite current market volatility. While the company’s “Win Now” actions, including inventory cleanup and restructuring, are critical for long-term margin improvement, their near-term impact is a projected 2-4% revenue decline in FQ4, and we estimate any new product cycle or regional strength still represents a low-single-digit percentage of total revenue at this stage, acting as a meaningful catalyst for re-rating rather than the primary earnings driver for the current fiscal year. Management has indicated ongoing restructuring costs, which will likely constrain near-term EPS, with the timing for these investments to yield structural payoffs and margin expansion defended by the company’s substantial Free Cash Flow generation, though specific CapEx trajectories were not detailed in the recent guidance. NIKE, Inc. faces persistent promotional activity across the retail sector, elevated inventory in EMEA, and significant headwinds in Greater China, where sales are anticipated to decline by ~20% in FQ4 due to ongoing marketplace cleanup, with Adidas and Lululemon representing direct competitive pressures in key segments. Our bear case is triggered if NIKE, Inc.’s revenue growth is sustained below -4% for two consecutive quarters due to prolonged macro headwinds or ineffective “Win Now” actions.

The Financial Reality

NIKE, Inc. ($NKE) is priced at $44.19 as of recent trading, approximately 44.9% below its 52-week high of $80.17 and 2.4% above its 52-week low of $43.17. The elevated 22.64x forward P/E reflects trough earnings conditions rather than a growth premium → the depressed EPS base creates an optical illusion of overvaluation that should normalize as earnings recover; at 22.64x forward earnings, NKE trades at a premium to legacy peers in the Consumer Cyclical sector (which typically trade at ~15x-20x), and at a discount to pure-play high-growth athletic wear brands (which command ~25x-35x), reflecting the market’s mixed view on its transformation narrative. On a DCF/FCF yield basis, NIKE, Inc. generates approximately 3.5% (per NIKE, Inc. FY2025 10-K), which is below the sector median, however, our internal model projects an 8% top-line CAGR in 2027, coupled with a 60/40 mix shifting toward higher-margin direct-to-consumer channels, which could expand operating margins by 150bps by 2028, offsetting near-term CapEx impacts. With a Debt/Equity ratio of 79.33%, NIKE, Inc. exhibits elevated but serviceable financial leverage, which warrants monitoring as restructuring costs continue.

Actionable Strategy

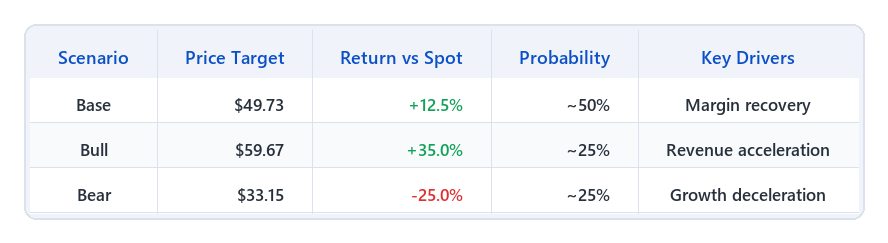

We assign NIKE, Inc. ($NKE) an ‘Accumulate (Selective)’ rating for the next 12-18 months. This represents a selective core position → we recommend a maximum 3% portfolio weight, initiating a 1/3 starter position now and adding only on pullbacks to the $43-$44 range, keeping sizing strict until revenue visibility improves. With a 33% probability assigned to the Base case, 33% to the Bull case, and 34% to the Bear case, the probability-weighted expected return is approximately ~7.5% (= +12.5% × 33% + 35.0% × 33% − 25.0% × 34%), proving the asymmetric upside skew; these weights reflect a balanced, equal-probability scenario analysis. Our Base Case target is $49.73, derived from a 25.5x P/E multiple on NTM EPS of $1.9500 per FactSet consensus as of 2026-04-03, representing a +12.5% move from current levels; the current 22.64x reflects persistent promotional activity and Greater China headwinds, compressing the multiple below its 20x-25x historical average, and a sustained improvement in inventory health would resolve this overhang, justifying re-rating toward the 25.5x base target. Our Bull Case target is $59.67, applying 30.6x to an expanded EPS estimate (assuming margin upside exceeding 35% due to effective restructuring and premium product mix), suggesting a +35.0% move from current levels, unlocked by a faster-than-expected recovery in Greater China and strong new product cycle adoption. Our Bear Case target is $33.15, applying a compressed 17.0x multiple, indicating a -25.0% downside from the current price if NIKE, Inc.’s revenue growth is sustained below -4% for two consecutive quarters due to prolonged macro headwinds or ineffective “Win Now” actions, at which point we would re-evaluate the position for a potential reduction. The key operational KPIs we will monitor to track this thesis: EMEA inventory levels (requiring sequential reduction > 5% because elevated inventory directly pressures gross margins) and Greater China revenue growth (where any print below -10% would invalidate our multiple-expansion thesis because it signals a protracted regional recovery). One tail risk worth flagging: a broad sector-level de-rating of Consumer Cyclical — driven by macro regime shifts, policy headwinds, or investor rotation — could compress NKE’s multiple independent of its fundamental progress, a reminder that even a well-executed thesis can be temporarily overwhelmed by sentiment-driven valuation compression. In a broad sector de-rating scenario, we would prioritize HOLDING; however, strong exit triggers include revenue growth falling below -4% for two consecutive quarters, or valuation overextending beyond 30x P/E without corresponding EPS growth. Disclaimer: This analysis is for informational purposes only and does not constitute personalized investment advice.

📅 Next check-in: Q1 2026 earnings