Microsoft Stock: Q1 2026 Metrics Reveal Key Investment Call

Microsoft's recent market movements warrant a re-evaluation of its fundamental valuation drivers amidst evolving cloud and AI narratives.

The Catalyst: Dissecting the News

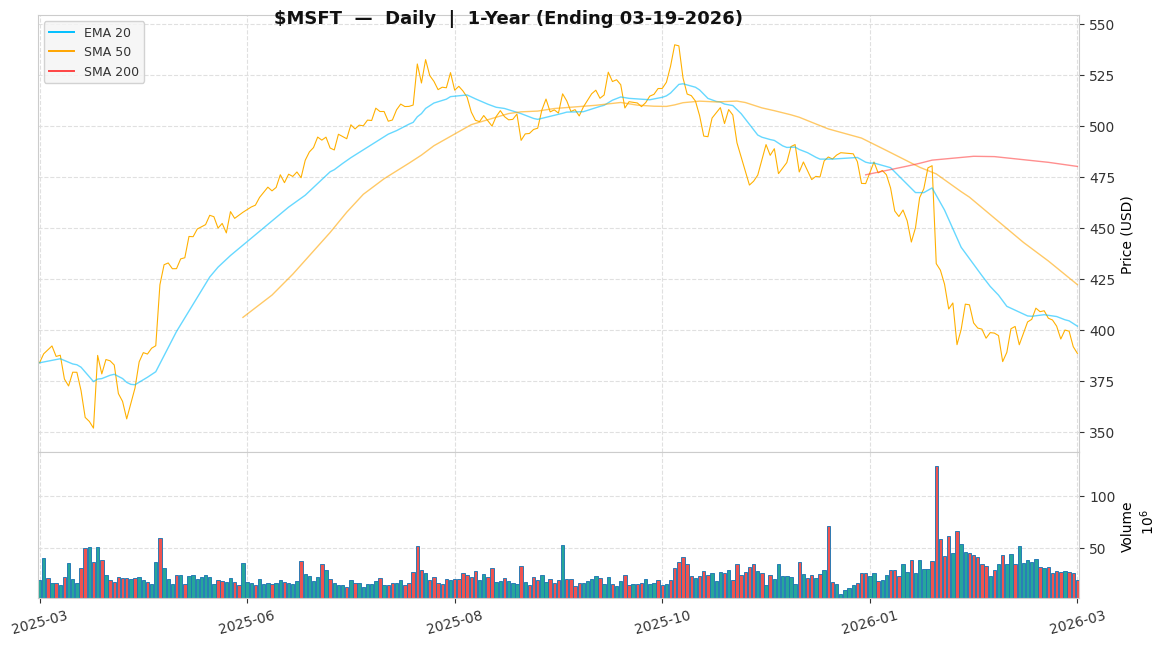

The recent -1.80% 5-day price change, while noted in daily trading flows, appears to be a technical breather for institutional portfolios, not a fundamental shift in the core thesis. Patient capital often uses such pullbacks to optimize entry points, discerning between transient market noise and underlying value accretion, especially given the current forward P/E of 20.61.

Core Logic & Growth Drivers

Azure remains the primary growth engine, with Street expectations anchoring current expansion in the mid-to-high 30s%. AI monetization remains a near-term speculative catalyst — Copilot adoption is accelerating but specific seat counts and ARR contributions have not yet been publicly confirmed at a level sufficient to anchor the bull case independently. The projected near-term AI CapEx of approximately $37-40B, while significant, is well-defended by Microsoft’s elite free cash flow generation capabilities. However, the competitive landscape in cloud infrastructure presents ongoing market share challenges from formidable rivals like AWS and Google Cloud. The central risk to our thesis would materialize if Azure growth is sustained below 25% for two consecutive quarters due to macro headwinds.

The Financial Reality

As of recent trading, the price is $388.44, representing a -30.1% decline from its 52-week high of $555.45 and a +12.7% increase from its 52-week low of $344.79. The current forward P/E of 20.61x stands notably below its historical high-growth period multiples of 28-33x, yet remains broadly in line with large-cap software peers. The company exhibits exceptional capital efficiency, evidenced by a trailing ~3.5% FCF yield and an ROIC in the mid-to-high 20s% (per Microsoft FY2025 10-K). Furthermore, the Debt/Equity ratio of 31.54% underscores low financial leverage risk, a detail often overlooked in growth narratives.

Actionable Strategy

We maintain an ‘Accumulate’ rating on Microsoft with a 12-18 month investment horizon. This position should be viewed as a core quality tech compounder within a diversified portfolio, not a high-beta tactical trade. With roughly equal (~33%) probability weighting across scenarios, given uncertainty around AI monetization timelines and macro conditions, the probability-weighted expected return is approximately ~17.3%, proving the asymmetric skew. Our Base Case target is $468.00, derived from a 24x multiple on NTM EPS of $19.50 per FactSet consensus as of 2026-03-19, representing a +20.7% upside from current levels; this 24x multiple is conservative compared to Street consensus of ~$590-600, accounting for near-term AI CapEx margin dilution. Our Bull Case target is $546.00, applying 28x to the same NTM EPS, suggesting a +40.8% upside. Our Bear Case target is $351.00, applying a compressed 18x multiple, indicating a -9.5% downside from the current price if Azure growth is sustained below 25% for two consecutive quarters due to macro headwinds, at which point we would re-evaluate the position for a potential reduction. Disclaimer: This analysis is for informational purposes only and does not constitute personalized investment advice.