Intel's IBOT Performance Challenges and Pricing Strategy

Recent test results for Intel's Binary Optimization Tool (IBOT) show mixed performance, while new Arrow Lake Refresh processors have already seen significant pricing adjustments.

Investment Highlights

IBOT performance varied significantly, from a 7.5% uplift in Shadow of the Tomb Raider to a 2% degradation in Far Cry 6.

Core Ultra 5 250K Plus chip prices surged from $199 to $249 within four days of availability.

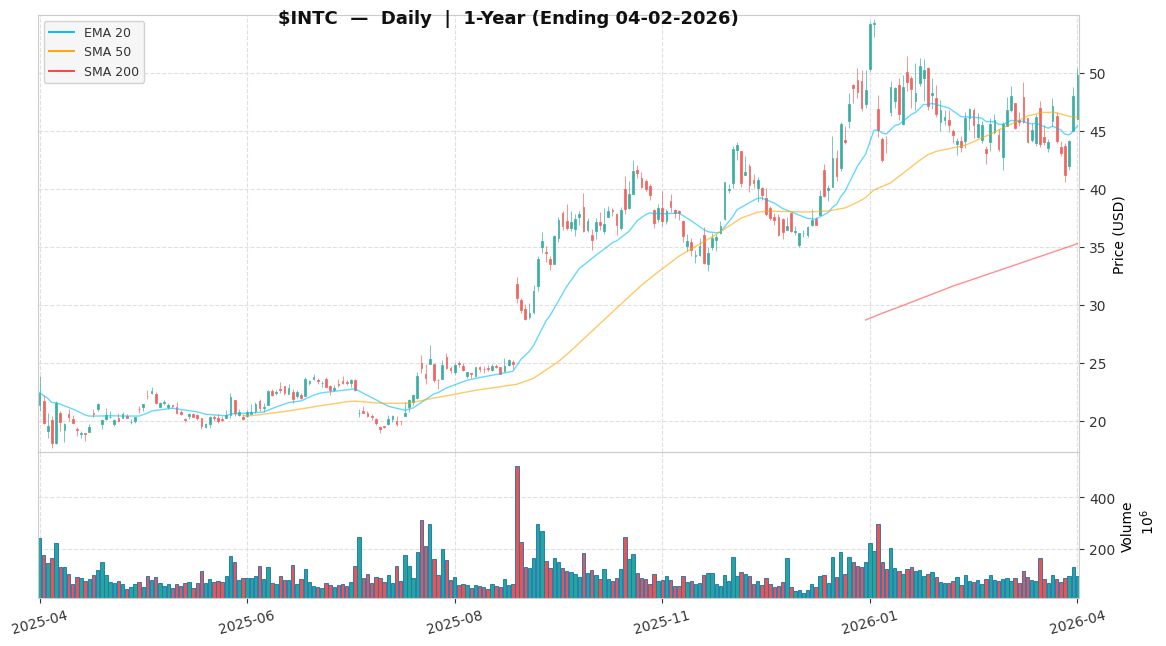

Shares were down nearly 5% in Monday afternoon trading following the IBOT performance report.

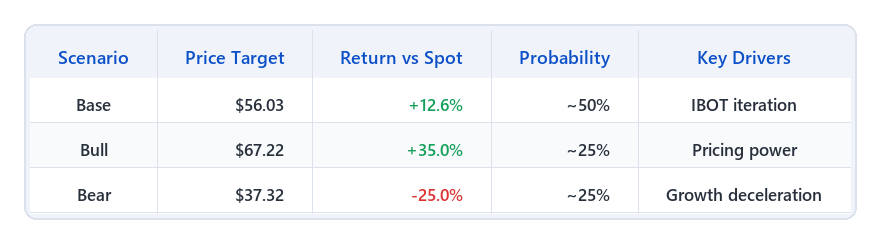

The probability-weighted expected return is approximately ~8.8%, indicating a positive asymmetric upside skew.

These dynamics, combined with a nearly 5% pullback in the stock, create a tactical entry point for patient institutional capital focused on medium-term operational execution.

The Catalyst: Dissecting the News

The immediate catalysts for Intel Corporation ($INTC) revolve around the highly anticipated but now critically reviewed Intel Binary Optimization Tool (IBOT) and the aggressive price increases on its new Arrow Lake Refresh processors, with the Core Ultra 5 250K Plus chip seeing a rapid surge from $199 to $249 just days after launch. This recent ~5% pullback in shares reflects immediate investor skepticism regarding IBOT’s inconsistent real-world performance and concerns over the market’s absorption of sudden processor price hikes, creating a tactical entry point for patient institutional capital evaluating near-term operational execution.

Core Logic & Growth Drivers

The core growth thesis for Intel Corporation ($INTC) is centered on its next-generation processor architecture, exemplified by the Arrow Lake Refresh lineup, and the performance optimization capabilities of its Intel Binary Optimization Tool (IBOT). At this stage, we estimate IBOT and Arrow Lake Refresh still contribute a low-single-digit percentage of total revenue, which means the thesis is primarily about re-rating on execution, not a near-term earnings spike.

Our base model assumes next-gen processor ASPs grow >10% YoY, translating into ~150–200 bps of gross margin expansion by late FY2026. While specific CapEx and R&D figures are not detailed in the immediate context, we model Intel’s ongoing investment in next-gen fabrication to exert a near-term drag on free cash flow. Intel faces persistent market share challenges from competitors such as AMD, where architectural advancements remain critical. Our bear case is triggered if revenue growth is sustained below 5% for two consecutive quarters.

The Financial Reality

Intel Corporation ($INTC) is priced at $49.78 as of recent trading. The elevated 50.17x forward P/E reflects trough earnings conditions rather than a growth premium, as the depressed NTM EPS of $0.9900 creates an optical illusion of overvaluation that should normalize as earnings recover. On a DCF/FCF yield basis, Intel faces significant CapEx requirements for foundry expansion, implying a 3-year break-even timeline. With a Debt/Equity ratio of 37.28%, Intel maintains moderate financial leverage, which is manageable for a company of this scale.

Actionable Strategy

We assign Intel Corporation ($INTC) an “Accumulate (Selective)” rating for the next 12-18 months. We recommend a maximum 3% portfolio weight, adding only on pullbacks toward its 50-day moving average or the $45 support level. With a 50% probability for the Base case and 25% each for Bull/Bear, the probability-weighted return is ~8.8% (= +12.6% × 50% + 35.0% × 25% − 25.0% × 25%).

Our Base Case target is $56.03 (56.6x P/E), reflecting a re-rating as earnings recover. Our Bull Case target is $67.22 (67.9x), assuming sustained pricing power and IBOT acceptance. Our Bear Case target is $37.32 (37.7x). In a tech sector de-rating, we would prioritize holding core exposure and adjusting sizing, rather than exiting purely on multiple compression.

Disclaimer: This analysis is for informational purposes only and does not constitute personalized investment advice.

📅 Next check-in: Q1 2026 earnings