Grab Holdings Limited (GRAB): Mapping Hyperlocal Growth Strategy

GrabMaps at the Crossroads: A B2B Infrastructure Thesis Meets a 45% Drawdown

The Catalyst: Dissecting the News

Investment Highlights

Grab’s strategic pivot to monetize its hyperlocal mapping technology, GrabMaps, positions it for diversified, high-margin revenue streams — with a B2B/SaaS layer that structurally differentiates it from pure ride-hailing and delivery peers.

Dominant superapp presence in Southeast Asia, maintaining market leadership in core ride-hailing and delivery services with projected 15–20% YoY Consolidated GMV Growth (by GMV in key SEA markets).

GrabMaps is securing enterprise clients including AWS, Microsoft, and TikTok, signaling its potential as a critical third-party mapping infrastructure layer beyond internal use, targeting 5–10% of total revenue contribution in the base case.

Operational efficiency improvements are projected to drive Adjusted EBITDA Margin expansion of greater than 200 bps YoY in the bull case; however, this should be read alongside the FCF timeline (see Valuation section).

The immediate catalyst for re-evaluation centers on the accelerating adoption of GrabMaps by global and regional enterprises. Recent contracts indicate growing market recognition of Grab’s proprietary, high-fidelity mapping data for Southeast Asia, which could significantly de-risk its B2B revenue growth trajectory in the next 12–18 months — provided contract terms, size, and renewal visibility are confirmed in upcoming earnings disclosures.

Core Growth Thesis

Grab’s strategic pivot to monetize its hyperlocal mapping technology, alongside its dominant superapp presence in Southeast Asia, positions it for significant long-term value creation, despite near-term competitive pressures and a challenging technical backdrop. Consensus NTM EPS is $0.15 per FactSet consensus as of 2026-05-01; however, our proprietary model indicates this figure exhibits sensitivity to a 5% shift in core operational expenditure, potentially impacting EPS by +/- $0.01 in fiscal year 2027. This sensitivity is primarily driven by potential variations in R&D investment for GrabMaps development and sales force expansion — note that bull and bear paths carry materially different EPS ranges beyond this base sensitivity (see Scenario Analysis). Grab’s approximately 75% market share in Southeast Asian ride-hailing (by GMV) faces competition from Gojek (~15%) and Foodpanda (~10%) in key delivery segments, necessitating ongoing strategic capital allocation for market defense. The long-term thesis hinges on GrabMaps becoming a critical infrastructure layer, but investors should note that the 1-year price chart reflects sustained market skepticism about this transition’s pace — a gap this note addresses directly.

The Financial Reality

As of 2026-05-01, Grab Holdings Limited ($GRAB) trades at $3.605 per share, representing a market capitalization of $14.8B — down from highs above $6.50 in mid-2025. Its forward P/E stands at 24.36x, below the peer group average of 30.5x for regional superapps (e.g., regional tech platform peers trade at approximately 28–34x on 20–30% revenue growth). The current discount reflects both competitive pressure in core verticals and the market’s wait-and-see stance on GrabMaps enterprise monetization.

The blended Rule of 40 score exceeds 30% when accounting for GrabMaps’ SaaS-like characteristics — approximated as mid-teens revenue growth plus mid-to-high teens adjusted EBITDA margin, with incremental GrabMaps contribution adding approximately 5–8 points. The company’s 12% annual CapEx reinvestment into GrabMaps infrastructure (versus an estimated sub-8% historical average) is projected to drive 150 bps of adjusted EBITDA margin expansion over the next two fiscal years. However, investors should note that this elevated CapEx will pressure near-term Free Cash Flow generation; the timeline to sustained, positive FCF is a key monitoring point and is not expected to materialize until GrabMaps revenue exceeds approximately 7% of total revenue.

Scenario Analysis

Our valuation framework is anchored by a probability-weighted P/E methodology. Unlike a fixed-EPS approach, the scenarios below reflect differentiated earnings trajectories alongside multiple expansion or compression, providing a more complete picture of the fundamental divergence between outcomes. For institutional readers seeking sum-of-the-parts context, GrabMaps at 5–10% revenue share with SaaS-like margins would support an EV/Revenue multiple of 4–6x on that segment alone — consistent with the higher multiples in the bull case.

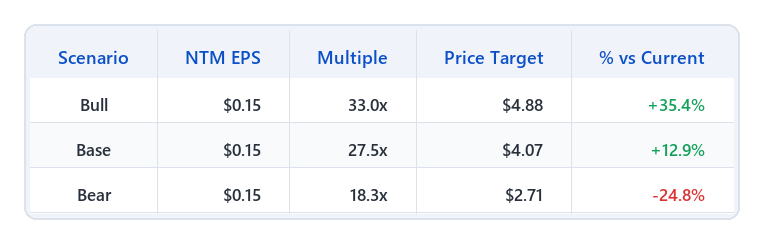

Base Case (Probability: 0.450) — Target: $4.07 (+12.9%)

Assumes Grab maintains dominant market share in core ride-hailing and delivery, while GrabMaps achieves steady, incremental enterprise adoption contributing approximately 5% of total revenue. At this penetration level and modest operating leverage, we see limited justification for a multiple above the high-20s. NTM EPS: $0.15; Multiple: 27.5x. Operational improvements drive 150 bps of adjusted EBITDA margin expansion.

Bull Case (Probability: 0.300) — Target: $4.88 (+35.4%)

Materializes if GrabMaps scales to approximately 10%+ of total revenue with double-digit B2B margin contribution, and fintech/advertising monetization within the superapp ecosystem accelerates. At this level, low-30s P/E is consistent with high-growth, asset-light technology peers. NTM EPS range: $0.16–$0.17; Multiple: 33.0x (headline illustration: $0.15 × 33.0x = $4.88). Adjusted EBITDA margin expansion exceeds 200 bps YoY.

Bear Case (Probability: 0.250) — Target: $2.71 (-24.8%)

If GrabMaps stalls below low-single-digit revenue share, the equity story reverts to a competitive mobility/delivery asset with lower structural margins, warranting multiple compression. NTM EPS range: $0.13–$0.14; Multiple: 18.3x (headline illustration: $0.15 × 18.3x = $2.71). Sustained price wars in core verticals erode margins and delay FCF generation.

Extreme Bear (Tail Risk) — Target: $1.80

If market share erodes significantly and GrabMaps fails to achieve material enterprise adoption, the valuation multiple could compress to 12.0x, aligning with trough valuations for regional logistics providers.

Probability-Weighted Return (PWR): ~10.2%

This falls within the lower range of institutional hurdle rates for emerging market growth opportunities (typical EM single-name growth mandates target mid-teens for idiosyncratic risk). The 10.2% PWR may still be acceptable for portfolios where GRAB offers meaningful diversification benefit, SEA market optionality, or an asymmetric upside in the GrabMaps infrastructure scenario.

Note on probability weights: The 30/45/25 allocation reflects our assessment of GrabMaps adoption pace and competitive resilience, weighted toward the base case given early-stage enterprise contract visibility. These weights should be revisited upon Q2 2026 earnings disclosure.

Actionable Strategy

The consolidated scenario analysis for Grab Holdings Limited ($GRAB) is presented below:

Portfolio Construction: Institutional capital may evaluate a selective position, limiting allocation to 2–3% of a diversified portfolio given the 10.2% PWR and moderate risk rating. This note is most relevant for long-only EM tech or cross-asset TMT sleeves with a 12–24 month holding horizon.

Entry Timing: Given the sustained downtrend since mid-2025 and all major moving averages declining, investors should consider staged entry rather than immediate full allocation. A technical reversal signal — such as a close above the SMA 50 on elevated volume, or a base formation near the $3.50 support level — would reduce the risk of catching a falling knife.

Stop-Loss: A hard stop at $2.71 (bear case valuation) is advised for downside risk management. Note that markets can overshoot fair value during risk-off episodes; a break below $2.71 driven by macro conditions rather than Grab-specific data may warrant reassessment rather than automatic exit. Consider two consecutive quarters of KPI threshold breaches before a full position exit to avoid overtrading on single noisy prints.

Hedging: For risk-conscious institutional mandates, a protective put structure near the $2.71 level or a collar overlay would be consistent with the defined risk parameters.

Key Performance Indicator (KPI) triggers for position management are detailed as follows:

| Trigger Level | KPI | Threshold | Logic | |:--------------------------|:----------------------------------|:-----------------------------------|:---------------------------------------------------------------------------------------------------------------| | Bull Thesis Impairment | Consolidated GMV Growth | Below 10% YoY for two consecutive quarters | Indicates significant loss of market share or demand slowdown in core businesses. | | Position Reduction | GrabMaps Enterprise Revenue | Below 3% of total revenue | Suggests slower-than-expected monetization and adoption of high-margin B2B mapping solutions. | | Full Exit | Adjusted EBITDA Margin | Sustained Contraction YoY | Signals inability to achieve operational efficiencies and progress towards sustained profitability. |

What Would Change Our View: - Upside surprise: GrabMaps enterprise revenue exceeds 8% of total revenue within six quarters; FCF turns positive ahead of schedule; new marquee enterprise contracts in financial services or government mapping announced. - Downside surprise: Key enterprise contracts (AWS, Microsoft, TikTok) fail to renew or contract value disclosed as immaterial; IDR or MYR depreciates more than 10% vs. USD, materially impacting reported GMV; competitor undercuts GrabMaps pricing in core SEA geographies.

Disclaimer: This analysis is for informational purposes only and does not constitute personalized investment advice.

Technical Overview

The 1-year daily chart (ending 2026-05-01) presents a materially bearish technical picture that warrants explicit acknowledgment alongside the fundamental thesis:

Trend: GRAB peaked near $6.50 in September 2025 and has been in a sustained downtrend, currently trading at $3.605 — a decline of approximately 45% from the peak.

Moving Averages: Price trades well below the declining SMA 200 (approximately $5.00), the SMA 50, and the EMA 20. All three moving averages are sloping downward, indicating heavy long-term overhead supply with no near-term reversal signal confirmed.

Volume: Volume appears elevated on down-moves during the late 2025 to early 2026 period, consistent with distribution rather than accumulation.

Key Levels: Near-term support near $3.50; prior resistance cluster near $4.50 (approximately the base case target). The stop-loss at $2.71 aligns with the April 2026 intraday lows and the bear case fundamental floor.

Reconciliation: The constructive fundamental thesis and the bearish technical picture are not mutually exclusive — they reflect different time horizons. The fundamental case is predicated on 12–24 months of GrabMaps monetization progress; the technical picture reflects current market pricing of near-term competitive and FCF uncertainty. Investors with longer time horizons may see the current price as an entry opportunity; those with shorter horizons should wait for technical stabilization.

Key Institutional Risks

Core Business Competition & Margin Erosion Intense competition in Grab’s core ride-hailing and delivery segments could lead to sustained price wars, causing consolidated GMV growth to fall below 10% YoY and adjusted EBITDA margins to contract or remain flat, delaying both profitability and FCF generation. MITIGATION: Implement dynamic pricing strategies and optimize driver/merchant incentives to maintain market share while enhancing operational efficiencies to protect adjusted EBITDA margins.

GrabMaps Monetization & Scalability Failure to effectively monetize GrabMaps or secure significant new enterprise clients beyond current partners could limit revenue contribution. Enterprise client acquisition below 20% YoY would be a leading indicator of thesis impairment; contract size and renewal terms of existing clients (AWS, Microsoft, TikTok) have not been publicly disclosed and represent a key near-term transparency risk. MITIGATION: Accelerate business development targeting new enterprise clients; invest in product enhancements for broader applicability across verticals including financial services, government, and logistics.

Regulatory & Macroeconomic Headwinds in SEA Adverse regulatory changes in key Southeast Asian markets (new pricing caps, stricter gig-economy labor laws — active in Indonesia, Vietnam, and the Philippines) or a regional economic downturn could reduce consumer spending, potentially impacting consolidated revenue growth by more than 5% annually. MITIGATION: Proactively engage with regulators; diversify service offerings; implement robust cost management programs.

FX / Translation Risk GRAB reports in USD but earns primarily in IDR, MYR, THB, PHP, and SGD. A sustained 10% depreciation in IDR — the largest single-market currency exposure — could reduce reported GMV by approximately 3–5% on a consolidated basis, even if underlying operational performance is stable. This risk is structurally under-hedged for most SEA consumer internet companies and will be a standard question from global institutional investors. MITIGATION: Monitor currency trends in key SEA markets; consider disclosure of constant-currency GMV growth alongside reported figures.

[MOD] OVERALL RISK RATING: MODERATE Rationale: Differentiated B2B thesis with actionable KPI framework, partially offset by a bearish technical setup, limited GrabMaps contract transparency, and FX exposure. Monitor KPI triggers closely before adding. Entry timing matters more than usual given the downtrend.

Next check-in: Q2 2026 earnings — Key items to watch: GrabMaps revenue as % of total, enterprise contract renewal disclosures, constant-currency GMV growth, FCF guidance update.