Figma's Path to Profitability: A Deep Dive into $FIG

A re-evaluation of Figma's high-growth potential in the context of Anthropic's Claude Design entry, persistent stock-based compensation, and the imperative for GAAP profitability.

Investment Highlights

Figma’s Q4 FY25 revenue grew 40% YoY to $303.8M, exceeding guidance.

Q1 FY26 revenue guidance implies 38% YoY growth, demonstrating sustained product leadership — but the trajectory must now be evaluated against a structurally altered competitive landscape.

Current $FIG valuation at $18.93 is -66.6% below its 52-week high of $56.79, reflecting a significant re-rating driven by both SBC concerns and emerging AI-substitution risk.

High Stock-Based Compensation (SBC) at 129.2% of revenue remains the primary drag on GAAP profitability.

[NEW — April 17, 2026] Anthropic’s launch of Claude Design — a dedicated AI-native design and prototyping platform powered by Claude Opus 4.7 — introduces a first-class structural competitive threat to Figma’s core workflow, elevating the Bear case probability and compressing the achievable forward multiple range.

The Catalyst: Dissecting the News

Figma, Inc. ($FIG) presents a compelling growth narrative in the creative design software sector, driven by robust product adoption and enterprise expansion. The immediate catalyst for a re-rating will be Q1 2026 earnings, where we monitor for any credible indication of decelerating Stock-Based Compensation (SBC) as a percentage of revenue or an accelerated path toward operating leverage. However, the analytical lens has materially widened since April 17, 2026: Anthropic’s launch of Claude Design — a research-preview AI-native platform for prototypes, slides, one-pagers, and marketing collateral, powered by Claude Opus 4.7 — represents not merely an incremental competitive development but a potential structural disruption to how design workflows are initiated and completed. Shares of $FIG were already under pressure ahead of the announcement on initial reports, confirming the market is explicitly repricing AI-substitution risk, not just GAAP/SBC dynamics. The stock’s -66.6% drawdown from its 52-week high of $56.79 therefore reflects both the valuation reset from persistent GAAP losses and an increasingly justified market discount for disruption risk — meaning the “entry point” narrative must be held with greater caution than our prior framing suggested.

Core Logic & Growth Drivers

The primary growth engine for Figma, Inc. ($FIG) continues to be its collaborative design platform, anchored by strong user engagement and expanding penetration into larger enterprise accounts. However, the character of Figma’s AI story has fundamentally changed in the past 24 hours: what we previously characterized as an emerging growth catalyst — Figma’s ‘AI Push’ driving adoption and multiple re-rating — must now be reframed as a defensive necessity. With Anthropic deploying Claude Opus 4.7 directly into design workflows, Figma’s AI capabilities are no longer a differentiating premium; they are the minimum required to retain existing customers. This is a qualitatively significant shift in our thesis.

Workflow overlap with Claude Design is not peripheral. Based on Anthropic’s published feature set, the overlap with Figma’s addressable use cases is substantial in the following segments:

High overlap (near-term seat pressure): Early-stage UX concepting, lightweight prototypes, marketing/PMM decks, landing pages, pitch presentations, and founder/PM “first draft” flows — all areas where Claude Design’s prompt-first interface could substitute for Figma seat usage.

Lower overlap (FIG-defensible near-term): Deep product design systems, multi-team component libraries, design system governance, versioning, developer handoff, and large-organization design ops — these workflows remain structurally complex in ways that AI-native tools do not yet address at enterprise scale.

Figma’s seat-based pricing model creates an additional vulnerability: if Claude Design and similar tools increase per-designer throughput, the enterprise’s required Figma seat count could decline even without users formally churning. This is a revenue compression mechanism that is distinct from and more insidious than traditional competitive churn.

Near-term, Figma’s operating fundamentals remain solid: $0.25B operating cash flow on $1.06B TTM revenue is genuinely healthy, and its position as the system of record for design collaboration at large enterprises is not erased overnight. However, non-cash SBC expenses continue to push GAAP net income to $-1.25B, and the competitive landscape now requires that R&D spend accelerate — which could further delay SBC normalization and GAAP profitability.

A note on the Anthropic partnership. Figma has previously partnered with Anthropic on developer workflow integrations. This relationship is now double-edged: it provides Figma with model access and distribution optionality, but it also means Figma has been a meaningful proving ground for Anthropic’s understanding of design workflows. Institutional investors will rightly ask whether Figma’s partnership helped a key supplier develop the domain knowledge required to forward-integrate into its core market.

The Financial Reality

Figma, Inc. ($FIG) is priced at $18.93 as of recent trading, approximately -66.6% below its 52-week high of $56.79 and +7.2% above its 52-week low of $17.65. The elevated 66.07x forward P/E reflects trough earnings conditions, but investors should no longer assume this optical cheapness normalizes on a clean trajectory: if the market reprices FIG’s terminal value lower due to AI-native disintermediation, the achievable normalized P/E band compresses materially. Where we previously anchored to a 35x–45x normalized range for high-growth SaaS in a rational market, we now believe a 25x–35x band is analytically appropriate if AI-native platforms capture a meaningful share of Figma’s lightweight workflow TAM — even with solid execution.

With SBC at 129.2% of TTM revenue, reported Non-GAAP EPS of $0.2900 excludes a real economic cost. Applying SBC as a full economic cost, we estimate GAAP-adjusted NTM EPS of ~$-2.42, implying a negative GAAP forward P/E materially higher than the Non-GAAP multiple. Investors relying solely on Non-GAAP metrics risk significantly overstating economic earnings power. For intrinsic value purposes, we model SBC as a full economic cost on GAAP FCF. The 3.87% Debt/Equity ratio indicates extremely low financial leverage risk.

The company’s Rule of 40 score (38% YoY revenue growth + estimated 10% Non-GAAP operating margin = 48%) remains healthy, but the PEG ratio (66.07x P/E / ~50% assumed NTM EPS growth = 1.32x) demands flawless execution on operating leverage. Post-Claude Design, the risk that execution proves less than flawless has meaningfully increased.

Actionable Strategy

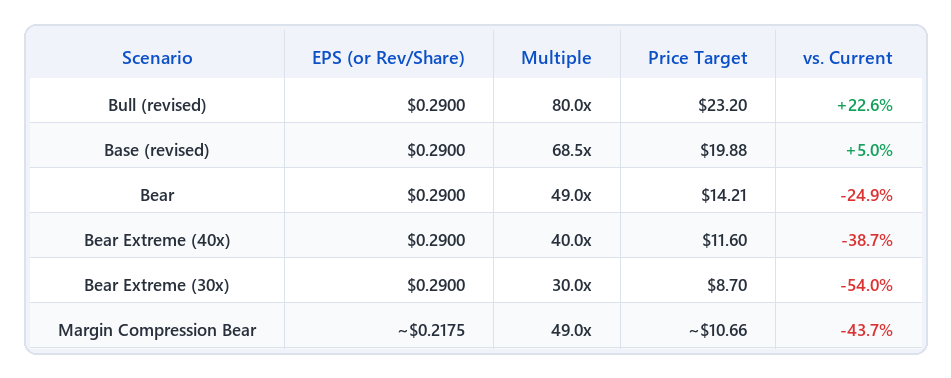

NTM EPS per FactSet consensus as of 2026-04-17 (GAAP-adjusted EPS for Margin Compression Bear is an estimate). Scenario probabilities revised to reflect Claude Design competitive development.

We maintain Figma, Inc. ($FIG) at an ‘Accumulate (Selective)’ rating for the next 12-18 months, but with materially increased caution. We recommend a maximum 2% portfolio weight (revised down from 3%), initiating a 1/3 starter position only on confirmed pullbacks to the $17.00–$18.00 range, and adding further only after Q1 2026 earnings provide credible evidence of: (a) SBC deceleration, AND (b) management’s articulation of a credible AI integration strategy that addresses the Claude Design threat. Investors who cannot tolerate the full bear range ($8.70–$14.21) should not initiate.

Revised scenario probabilities reflect the Claude Design development:

We now assign 30% to the Base case, 20% to the Bull case, and 50% to the Bear/Bear Extreme cases combined (35% Bear, 15% Bear Extreme), producing a revised probability-weighted expected return of approximately ~-1.8% (= +12.6% × 30% + 35.1% × 20% − 24.9% × 35% − 46.4% × 15%). The negative PWR does not invalidate the position entirely — asymmetric upside in the bull scenario and the possibility that the market overestimates near-term displacement speed justify a small satellite position — but it does confirm this is firmly a high-conviction watch, not a conviction buy at current prices.

Base Case target: $19.88 — revised from $21.31 — derived from a 68.5x P/E on NTM EPS of $0.2900. The multiple compression from 73.5x to 68.5x reflects the additional uncertainty introduced by AI-native competition, which justifies a structural discount to our prior base multiple. This represents a +5.0% move from current levels, and requires: continued >35% revenue growth, no evidence of seat count erosion from AI substitution, and a credible management AI roadmap by Q2 2026.

Bull Case target: $23.20 — revised from $25.58 — applying 80.0x to an expanded EPS estimate (vs. prior 88.2x). The multiple ceiling is lower because the bull scenario now requires Figma to not merely grow revenue, but to demonstrably integrate AI-native workflows — including Claude-style tools — into its platform rather than being displaced by them. This implies a +22.6% upside.

Bear Case target: $14.21, applying a compressed 49.0x multiple, indicating -24.9% downside if YoY revenue growth falls below 35% for two consecutive quarters. A specific AI-disruption path for the bear case: if Claude Design and similar tools capture a meaningful share of early-stage design workflows and Figma management does not articulate a credible integration response, revenue growth could structurally trend below 30–35%, permanently capping the achievable P/E band and validating a 25x–35x terminal multiple rather than 35x–45x.

Bear Extreme / Margin Compression scenarios remain unchanged at $8.70 (30x), $11.60 (40x), and ~$10.66 (49x on ~$0.2175 EPS), and we now consider these scenarios modestly more probable than before.

KPIs to monitor (updated): YoY Revenue Growth (must sustain >35%); Operating Cash Flow Margin (below 25% invalidates multiple expansion thesis); SBC as % of Revenue (QoQ increase for 2 consecutive quarters = valuation risk multiplier); [NEW] Enterprise Seat Retention Rate (any evidence of net seat count decline at existing enterprise accounts, however anecdotal, is an early AI-displacement signal requiring immediate thesis review); [NEW] Management AI Roadmap Credibility (Q1 2026 earnings call: does management specifically address Claude Design and articulate Figma’s response strategy? Absence of this is a negative signal).

Exit triggers: revenue growth below 30%; SBC as % of revenue increasing QoQ for 2 consecutive quarters; valuation overextending beyond 75x P/E without corresponding EPS growth; or evidence that enterprise customers are initiating workflows in AI-native tools rather than Figma.

Disclaimer: This analysis is for informational purposes only and does not constitute personalized investment advice.

🛡️ Key Institutional Risks

Excessive Stock-Based Compensation Figma’s SBC currently stands at 129.2% of revenue, driving substantial GAAP losses and significant shareholder dilution. This is unsustainable for institutional investment and now carries an additional complication: the competitive response to Claude Design may require accelerated R&D, further delaying SBC normalization. MITIGATION: Monitor SBC as a percentage of revenue. If it remains above 100% for two consecutive quarters without a clear reduction plan, reduce position size or place a hard stop. Require management to quantify the R&D response to AI competition separately from baseline SBC guidance.

Revenue Growth Deceleration Increased competition — now including AI-native platforms with foundational model capabilities — could cause Figma’s YoY revenue growth to fall below the 30% threshold, collapsing its premium valuation. MITIGATION: Establish a monitoring trigger: if quarterly YoY revenue growth falls below 30%, initiate a full thesis review and consider partial divestment. Pay particular attention to mix within revenue: if enterprise seat expansion slows while SMB growth holds, this is an early signal of AI displacement in the most profitable cohort.

Persistent GAAP Unprofitability Figma’s significant GAAP losses (Net Income TTM: $-1.25B, Profit Margin: -118.4%) driven by high SBC make its Non-GAAP forward P/E of 66.07x structurally fragile. The path to GAAP profitability is now more uncertain, as competitive pressure from AI-native tools may require sustained elevated R&D investment. MITIGATION: Require a credible management plan for achieving positive GAAP net income within 12-18 months. If no such plan emerges, or GAAP losses widen, reduce exposure to a predefined maximum percentage of the portfolio.

[NEW] AI-Native Disintermediation Risk Anthropic’s launch of Claude Design (April 17, 2026), powered by Claude Opus 4.7, introduces a direct AI-native competitor across Figma’s highest-volume lightweight workflows: prototypes, decks, one-pagers, wireframes, and marketing collateral. This is not a feature gap — it is a workflow substitution risk with a well-funded, frontier-model operator behind it. If AI-native tools capture a structurally meaningful share of new design projects, Figma’s seat expansion trajectory could compress even without explicit customer churn, as AI augmentation reduces the number of Figma seats required per design team. MITIGATION: Monitor: (a) Q1/Q2 2026 earnings commentary specifically addressing AI-native competitive response; (b) any reported changes in enterprise net seat expansion; (c) whether Figma integrates Claude or other foundational models into its core platform in a way that neutralizes substitution (i.e., Figma becomes the collaboration layer on top of AI-generated assets, rather than being bypassed). If management does not articulate a credible AI integration strategy within two earnings cycles, treat this as a structural thesis break and lower position weight accordingly. Reduce the achievable P/E target multiple from 35–45x to 25–35x in the normalized band.

🔴 OVERALL RISK RATING: HIGH (ELEVATED) Rationale: Forward P/E > 50x, persistent GAAP losses, and — as of April 17, 2026 — a direct AI-native competitive entry by Anthropic into Figma’s core workflow. The tail risk of AI-native disintermediation has migrated into the base risk scenario. Strict position sizing (≤2% portfolio weight) is mandatory. This is a satellite/asymmetric position only.

📅 Next check-in: Q1 2026 earnings (watch for AI competitive response language and SBC guidance)