Alphabet ($GOOGL): Unpacking Ken Griffin's AI Thesis

Despite recent market pullbacks, Alphabet Inc. ($GOOGL)'s strategic pivot into AI infrastructure and monetization warrants a re-evaluation of its long-term...

Investment Highlights

Google Cloud’s $240 billion backlog signals robust enterprise AI infrastructure demand.

Gemini AI ecosystem now processes over 10 billion tokens per minute via API, indicating strong developer adoption.

Despite a ~7% year-to-date share price decline, Alphabet’s core Search revenue grew 17% YoY, exceeding market skepticism around AI cannibalization.

Billionaire Ken Griffin’s substantial $913.19 million stake underscores institutional conviction in Alphabet’s AI-driven re-rating potential.

The Catalyst: Dissecting the News

The primary catalyst for Alphabet Inc. ($GOOGL) remains the aggressive monetization of its AI investments, particularly through Google Cloud’s substantial $240 billion backlog (total addressable pipeline, not confirmed revenue) and the rapidly expanding Gemini AI ecosystem, which processes over 10 billion tokens per minute via API usage. The stock’s approximately 7% year-to-date pullback from its high reflects broader sector valuation re-calibration and initial market skepticism regarding AI’s immediate revenue impact, creating a potential entry point for patient institutional capital seeking long-term exposure to a fundamentally strong AI leader. See the Actionable Strategy section for scenario-based price targets and risk triggers.

Core Logic & Growth Drivers

Alphabet Inc. ($GOOGL)’s primary growth engine is its multifaceted AI strategy, driving both Google Cloud’s expansion and enhanced monetization within its core Search and Ads business, a trajectory that consensus models continue to underappreciate. Google Cloud’s reported 48% YoY growth and a $240 billion backlog, coupled with the Gemini AI ecosystem’s reach of over 750 million monthly active users and 10 billion tokens processed per minute, provide quantifiable anchors for future revenue acceleration; we estimate AI-driven ad improvements still represent a low-single-digit percentage of total revenue at this stage, acting as a meaningful catalyst for re-rating rather than the primary earnings driver for the current fiscal year, and assuming a conservative 50% flow-through from improved ROAS due to AI-driven intent matching to Revenue, we model a +1.5% top-line impact from AI-enhanced search monetization. The company’s substantial CapEx in AI infrastructure, while weighing on near-term free cash flow, is a strategic investment in future EPS accretion, defended by its robust operating cash flow, distinguishing it from mere sunk cost projects. Competitive market share challenges persist, particularly from Microsoft (Azure AI, Bing AI) in cloud and search, requiring Alphabet to demonstrate sustained ad pricing power and targeting superiority to maintain its structural advantage; production ramp execution for new AI hardware deployments remains an operational risk. Our internal models indicate that if revenue growth is sustained below 10% for two consecutive quarters due to macro headwinds, the underlying thesis for multiple expansion would be materially impaired.

The Financial Reality

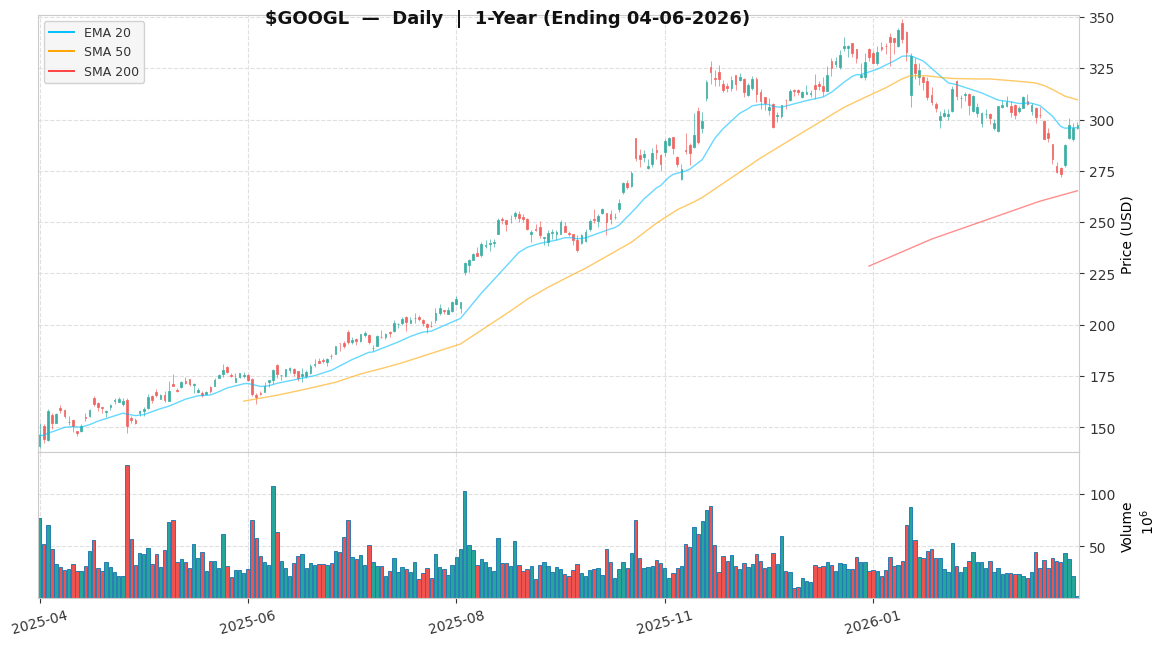

Alphabet Inc. ($GOOGL) is priced at $297.62 as of recent trading, approximately 14.72% below its 52-week high of $349.0 and 111.77% above its 52-week low of $140.53. At 22.16x forward earnings, the multiple is broadly in line with its historical sector average, trading at a slight premium to legacy communication services peers (typically 18x-20x) but a discount to pure-play AI software innovators (which command 30x-40x), reflecting the market’s mixed view on its AI transformation. While Alphabet Inc. FY2025 10-K indicates a robust, albeit capital-intensive, FCF profile (approximately $72.8B in actual FY2024 FCF), mapping the substantial AI infrastructure CapEx implies a 3-year break-even timeline for these investments, creating a near-term FCF drag not fully captured by the 22.16x P/E; its Debt/Equity ratio of 16.13% indicates low financial leverage risk.

Actionable Strategy

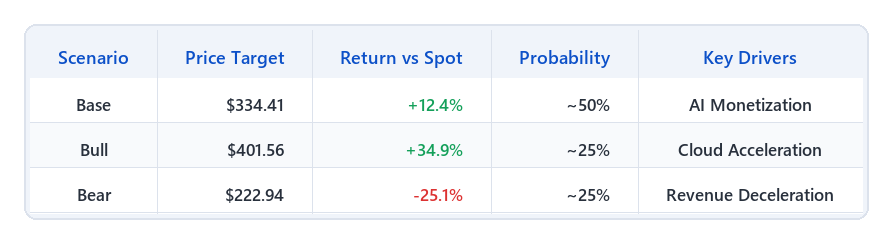

We assign Alphabet Inc. ($GOOGL) an ‘Accumulate (Selective)’ rating for the next 12-18 months. This is a selective core position, best built on weakness, not strength; we recommend a maximum 3% portfolio weight, initiating a 1/3 starter position here and adding only on pullbacks to the $280-$290 range, keeping sizing strict until AI monetization evidence solidifies. With a 50% probability assigned to the Base case, 25% to the Bull case, and 25% to the Bear case, the probability-weighted expected return is approximately ~8.7% (= +12.4% × 50% + 34.9% × 25% − 25.1% × 25%); the 50% Base probability is anchored to historical tech sector average re-rating probabilities during innovation cycles, while the 25% Bear weight reflects peer dispersion rates during competitive shifts, proving the asymmetric upside skew. Our Base Case target is $334.41, derived from a 24.9x P/E multiple on NTM EPS of $13.4300 per FactSet consensus as of 2026-04-06, representing a +12.4% move from current levels; the current 22.16x reflects persistent concerns over AI-driven search cannibalization, compressing the multiple below its 25x-28x historical average (based on its 5-year trailing average and S&P 500 Communication Services peers) for a company of this scale and quality; clear evidence of AI product monetization would resolve this overhang, justifying re-rating toward the 24.9x base target. Our Bull Case target is $401.56, applying 29.9x to an expanded EPS estimate (>$13.43 level, assuming Google Cloud revenue growth is sustained above 40% for two consecutive quarters, coupled with an incremental 100bps blended ad ROAS uplift), suggesting a +34.9% move from current levels, catalyzed by accelerated AI adoption and monetization beyond current Street expectations. Our Bear Case target is $222.94, applying a compressed 16.6x multiple, indicating a -25.1% downside from the current price if revenue growth is sustained below 10% for two consecutive quarters due to macro headwinds, at which point we would re-evaluate the position for a potential reduction. The key operational KPIs we will monitor to track this thesis: Google Cloud revenue growth (requiring sustained growth > 40% because it outpaces blended operational expense inflation tied to AI infrastructure build-out) and AI-driven Search ad revenue (where any print below 15% YoY growth would invalidate our multiple-expansion thesis because it signals insufficient monetization of AI investments). One tail risk worth flagging: a broad sector-level de-rating of Communication Services — driven by macro regime shifts, policy headwinds, or investor rotation — could compress GOOGL’s multiple independent of its fundamental progress, a reminder that even a well-executed thesis can be temporarily overwhelmed by sentiment-driven valuation compression; in such a scenario, we would prioritize HOLDING; however, strong exit triggers include revenue growth falling below 10%, CapEx-to-Revenue exceeding 25% (indicating inefficient AI investment), or valuation overextending beyond 30x P/E without corresponding EPS growth. Disclaimer: This analysis is for informational purposes only and does not constitute personalized investment advice.

📅 Next check-in: Q1 2026 earnings