Allbirds (BIRD) AI Pivot: A High-Stakes Compute Gamble

Allbirds, Inc. ($BIRD) undergoes a complete strategic re-evaluation as its pivot to GPU-as-a-Service positions it in a high-demand, high-risk sector,...

Investment Highlights

Allbirds, Inc. ($BIRD) divested footwear assets for $39M, signaling a full pivot from consumer retail.

NewBird AI secured $50M in convertible financing to acquire high-performance GPU assets for GPUaaS, targeting a market with “unprecedented structural demand.”

The stock surged +407.95% in five days, reflecting speculative market enthusiasm for the AI compute narrative.

The company transitions from a deeply unprofitable $-0.08B Net Income (TTM) consumer brand to an unproven AI infrastructure provider.

The primary catalyst driving Allbirds, Inc. ($BIRD) is its strategic pivot to NewBird AI, aiming to become a GPU-as-a-Service (GPUaaS) and AI-native cloud solutions provider, directly addressing the “unprecedented structural demand for specialized, high-performance compute” as noted in its recent regulatory filings. The company’s execution on initial GPU asset acquisition and securing long-term lease arrangements for compute capacity will be the immediate milestones to monitor in the next 1-2 quarters, particularly given the $50 million initial capital injection. The stock’s dramatic +407.95% 5-day price change off its 52-week low ($3.04) reflects intense speculative fervor and a rapid re-rating driven by the AI compute narrative, creating a highly volatile entry point for institutional capital attempting to front-run the AI infrastructure buildout.

The Catalyst: Dissecting the News

The primary catalyst and price action context are summarized in the Investment Highlights above. See the Actionable Strategy section for scenario-based price targets and risk triggers.

Core Logic & Growth Drivers

The primary growth engine for Allbirds, Inc. ($BIRD) is now its newly formed NewBird AI division, which plans to capitalize on the acute market shortage of high-performance GPU compute capacity by offering GPU-as-a-Service under long-term lease arrangements, a stark departure from its historical consumer retail operations. NewBird AI’s monetization remains a near-term growth catalyst; adoption is accelerating but specific figures have not yet been publicly confirmed at a level sufficient to anchor the bull case independently. We estimate NewBird AI still represents a sub-5% percentage of total revenue at this stage, acting as a meaningful catalyst for re-rating rather than the primary earnings driver for the current fiscal year, implying the investment thesis is primarily about a multiple re-rating on execution rather than a near-term earnings explosion.

The initial $50 million convertible financing facility is earmarked to acquire high-performance GPU assets, representing a significant upfront CapEx requirement which will create an immediate drag on operating cash flow (currently $-0.06B TTM) and is expected to be EPS dilutive in the near term until substantial revenue scale is achieved from GPUaaS contracts. Note: Key terms of the convertible facility — including conversion price, coupon rate, and maturity date — have not been publicly disclosed in sufficient detail. These terms represent a material disclosure gap; a conversion price near current market levels, for instance, could meaningfully alter the probability-weighted return calculus, and investors should seek full disclosure of these terms before sizing a position.

The GPUaaS unit economics at scale will be a critical determinant of whether this pivot creates durable value. Key drivers to monitor include: GPU cluster utilization rates (industry breakeven typically requires sustained utilization above 70%), per-GPU depreciation schedules (high-performance H100-class GPUs depreciate over 3-5 years, creating significant fixed cost drag before revenue ramp), and gross margin potential (specialized GPUaaS providers can achieve 40-60% gross margins at scale, but only with high utilization and efficient procurement — neither of which NewBird AI has demonstrated). Until these unit economics are observable, the bull case rests on market structure rather than company-specific evidence.

The GPUaaS market itself carries a “structural demand” narrative that warrants scrutiny. Hyperscaler capacity constraints are real, but the accessible portion of that market for a new, sub-scale entrant is a fraction of the headline TAM. NewBird AI’s realistic initial addressable segment is likely the mid-market enterprise and research institution segment that finds hyperscaler minimums too costly and specialized providers like CoreWeave too capacity-constrained — a real but narrow wedge. The reference to “unprecedented structural demand” is directionally correct but should not be taken as validation of NewBird AI’s specific market position within it.

NewBird AI faces intense competitive challenges from established hyperscalers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP), alongside well-funded specialized GPUaaS providers such as CoreWeave, all possessing superior capital resources and existing customer bases. A credible bull case requires a defensible differentiation vector — plausible candidates include geographic data sovereignty positioning, focus on a niche vertical (e.g., biotech, defense simulation, media rendering), or a hardware partnership that provides preferential GPU access. None of these has been publicly announced; their absence is the primary reason for a Speculative rather than outright Buy rating.

A note on management credibility: a pivot of this magnitude — from footwear retail to AI infrastructure — requires explicit evaluation of whether the leadership team has the technical and operational depth to execute. Public disclosures have not yet surfaced material evidence of domain expertise in GPU infrastructure buildout. This is a key due diligence item for any institutional investor before initiating a position.

Furthermore, given its pre-profitability stage, we assume at least one additional capital raise beyond the initial $50 million within the investment horizon, which could partially offset upside via dilution. Our bear case is triggered if NewBird AI fails to effectively procure and deploy high-performance GPUs, struggles to attract and retain significant customers against established hyperscalers, and exhausts its capital without achieving sustainable revenue or profitability.

The Financial Reality

Allbirds, Inc. ($BIRD) is priced at $12.14 as of recent trading, approximately 50.0% below its 52-week high of $24.31 and 300.7% above its 52-week low of $3.04. The -1.75x forward P/E reflects the company’s pre-profitability status, typical for early-stage companies in this sector, and is not a meaningful standalone valuation signal; at -1.75x forward earnings, Allbirds trades at a significant discount to established technology infrastructure peers and at a premium to its former consumer retail peers, reflecting the market’s mixed view on its transformation narrative.

Despite a negative operating cash flow of $-0.06B (TTM) and a profit margin of -50.7%, the company holds approximately $26.7M in cash, burning ~$13.8M per quarter (annualizing to ~$55M, consistent with the reported -$0.06B OCF figure), implying approximately 1.9 quarters of runway before additional capital is required. [Clarification: The -$0.08B net income figure cited in the Investment Highlights reflects a different earnings line than OCF; readers should verify both figures against the same TTM filing period to avoid conflation.] The 110.38% Debt/Equity ratio represents elevated but serviceable financial leverage, a risk factor warranting monitoring.

Actionable Strategy

We assign Allbirds, Inc. ($BIRD) a ‘Speculative Buy’ rating for the next 12-18 months, recognizing the binary nature of its strategic pivot. This is a high-risk, early-stage venture; sizing must reflect binary execution risk, and we recommend a maximum 1-2% of portfolio weight, initiating a 1/3 starter position now and adding only on pullbacks to the $10-$11 range, keeping sizing strict until GPU procurement and initial customer contract milestones are confirmed.

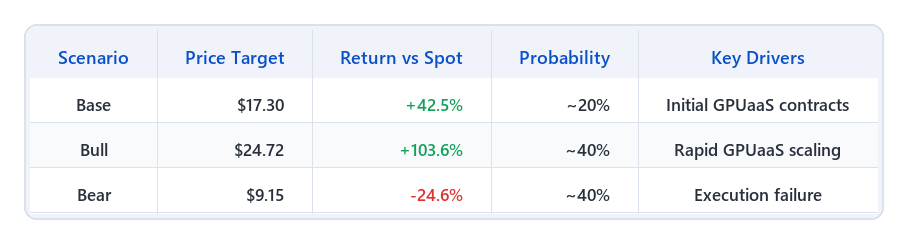

On scenario probability weighting: We deliberately assign 20% to the Base case, 40% to the Bull case, and 40% to the Bear case. This non-standard, bimodal distribution reflects our view that this pivot is genuinely binary in nature: the company will either achieve meaningful GPUaaS adoption — in which case the stock re-rates sharply — or it will exhaust capital without traction, in which case the downside is severe. In a business transformation of this magnitude, the median “muddle through” scenario is, in our assessment, the least probable outcome; companies pivoting from retail to infrastructure at this scale tend to succeed or fail decisively rather than stabilize in a middle state. Investors who prefer a more conventional distribution (e.g., 40% Base / 30% Bull / 30% Bear) should note that this yields a probability-weighted return of approximately +24.5% — still positive, but substantially more conservative than our base estimate.

With the above probability weights, the probability-weighted expected return is approximately ~40.1% (= +42.5% × 20% + 103.6% × 40% − 24.6% × 40%). Readers should note that this figure is highly sensitive to the bull-case weighting: the bull scenario contributes ~41.4 percentage points to the total, making it the dominant driver. If the bull case probability is revised downward to 25%, the expected return falls to approximately +8.5%. We present this sensitivity explicitly to ensure full transparency in the risk/reward framework.

Base Case target: $17.30, representing a +42.5% move from current levels, derived from a 0.7x P/S multiple applied to TTM Revenue per Share of $24.72 (per yfinance, as of 2026-04-16).

Valuation methodology and caveat: The TTM revenue base used here reflects Allbirds’ legacy footwear business, which has been divested. Applying a GPUaaS infrastructure multiple to footwear revenue is an imperfect placeholder, used because NewBird AI has not yet generated sufficient GPUaaS revenue to support a forward model. A more rigorous approach — which we recommend this analysis adopt in future updates once GPUaaS revenue becomes reportable — would build a forward estimate anchored in unit economics: (number of GPU clusters deployed) × (utilization rate) × (price per GPU-hour) × (hours per year), stress-tested across utilization scenarios of 50%, 70%, and 90%. Until such a model is supportable, the TTM-based P/S target should be treated as an order-of-magnitude anchor rather than a precise fair value.

The P/S multiple range of 0.37x–1.0x draws on early-stage growth OEM precedents as a conservative placeholder in the absence of direct public comparables at this revenue scale. We acknowledge this is an imperfect analogy: a GPUaaS business at scale is structurally closer to a cloud infrastructure provider, with potentially higher gross margins than a hardware-dependent OEM. More appropriate long-run comparables would include specialized cloud compute providers and infrastructure-as-a-service businesses; as NewBird AI’s business model becomes observable, the multiple framework should be updated accordingly.

Bull Case target: $24.72 (+103.6%), applying 1.0x to an expanded revenue estimate, assuming NewBird AI rapidly scales its GPUaaS infrastructure, leverages its $50M financing effectively to acquire high-demand GPUs, and secures multiple large, long-term enterprise contracts. The 1.0x multiple reflects the re-rating potential if the company demonstrates sustained gross margin improvement and revenue acceleration.

Bear Case target: $9.15 (-24.6%), applying a compressed 0.37x multiple, indicating downside from current price if NewBird AI fails to effectively procure and deploy high-performance GPUs, struggles to attract and retain significant customers against established hyperscalers, and exhausts its capital without achieving sustainable revenue or profitability. The 0.37x multiple reflects distressed sector valuations in a scenario of persistent cash burn and deteriorating investor confidence.

Key operational KPIs to monitor: - GPUaaS Annualized Recurring Revenue (ARR): Requires sustained growth >$20M annually to signal market adoption and revenue viability - Cash Runway: Any print below 2 quarters invalidates our multiple-expansion thesis - GPU Cluster Utilization Rate: Must exceed 70% on deployed clusters to validate unit economics - GPUaaS Gross Margin: A sustained margin below 30% would indicate pricing pressure or procurement inefficiency inconsistent with the bull case

One tail risk worth flagging: a broad sector-level de-rating of AI infrastructure — driven by macro regime shifts, policy headwinds, or investor rotation — could compress BIRD’s multiple independent of its fundamental progress, a reminder that even a well-executed thesis can be temporarily overwhelmed by sentiment-driven valuation compression. In a broad sector de-rating scenario, we would prioritize HOLDING; however, strong exit triggers include GPUaaS ARR falling below $10M for two consecutive quarters, or cash runway falling below 1 quarter.

On timeline realism: The 12-18 month investment horizon assumes NewBird AI can progress from GPU procurement through initial customer contracts to early ARR visibility within that window. This is an aggressive timeline that assumes no significant supply-chain delays in GPU procurement (H100-class GPUs have historically carried extended lead times), no major customer acquisition setbacks, and successful execution of at least one additional capital raise. Investors should treat the 12-18 month window as a milestone checkpoint, not a guaranteed outcome horizon.

Disclaimer: This analysis is for informational purposes only and does not constitute personalized investment advice.

Sensitivity note: Revising bull probability to 25% yields a PWR of ~+8.5%. Revising to 30% yields ~+24.5%. Readers should apply their own probability assessment to the scenario table above.

🛡️ Key Institutional Risks

🔴 OVERALL RISK RATING: HIGH

Rationale: The combination of ~1.9 quarters of cash runway, zero GPUaaS revenue history, no demonstrated management expertise in AI infrastructure, severe hyperscaler competition, and a convertible financing structure with undisclosed terms constitutes a high-risk profile by institutional standards. The “Speculative Buy” rating reflects a positive probability-weighted expected return under specific scenario assumptions — not a low-risk entry. Position sizing must reflect this accordingly.

AI Pivot Execution Failure The company’s complete lack of prior experience in AI infrastructure and GPUaaS makes successful execution highly uncertain. Failure to secure initial GPU supply or significant customer contracts (>$10M ARR) within 9 months would confirm this risk. Milestones required to disprove: first GPU cluster operational announcement; first signed enterprise customer contract with disclosed ARR.

MITIGATION: PM should establish a strict monitoring threshold for key operational milestones (e.g., first GPU cluster operational, first customer contract signed) and exit the position if no significant GPUaaS contracts (>$10M ARR) are announced within 9 months.

Capital Depletion & Dilution Given the capital-intensive nature of GPUaaS and BIRD’s history of negative cash flow ($-0.06B OCF TTM), the initial $50M financing is likely insufficient, leading to rapid capital depletion and severe shareholder dilution if cash runway falls below 1 quarter. The undisclosed terms of the convertible note compound this risk materially: if conversion is triggered at or near current market prices following the 407% move, dilution could be substantially larger than a simple share-count estimate implies. Investors should request or await full convertible note term disclosure before committing full position size.

MITIGATION: PM must monitor the company’s cash balance and burn rate quarterly. If the cash runway drops below 2 quarters without substantial new, non-dilutive financing or significant revenue generation, the position should be exited.

Competitive Disadvantage NewBird AI enters a highly competitive market dominated by established hyperscalers and specialized providers with superior resources, existing customer bases, and economies of scale. Without a clear, defensible differentiation — such as geographic data sovereignty positioning, a niche vertical focus, or a preferential hardware supply arrangement — BIRD will struggle to acquire and retain customers, leading to minimal market share and revenue.

MITIGATION: PM should require clear evidence of customer acquisition (e.g., >5 significant customer contracts within 12 months) and a defined competitive moat (e.g., specialized hardware, unique software stack, or niche market dominance) to maintain the position.

📅 Next check-in: Q2 2026 earnings